How do hedge funds work (and should I invest in them)?

I recently stumbled onto an article about hedge funds. It wasn’t the most flattering article. It explained how hedge fund performance is actually far worse than what you’d think.

I rarely get any serious questions about hedge funds. I do periodically hear of investors wanting to liquidate them. Unfortunately most hedge fund investors don’t quite know what they’ve gotten themselves into.

What is a hedge fund?

Let’s start with what a hedge fund is. Like mutual funds or any other investment for that matter, the goal of a hedge fund is to produce a positive rate of return on your investment. Unlike mutual funds hedge funds ARE NOT regulated by the SEC (though the may very well be regulated soon).

Their is a big difference between hedge funds and most other investments. Hedge funds have much broader parameters on what they can and cannot do with your money.

Many hedge funds invest in traditional stocks or bonds. Typically they use more aggressive and leveraged tactics to do so. Other hedge funds use more sophisticated (and far riskier) investments and strategies.

How do hedge funds invest my money?

The strategies a hedge fund uses to invest your money vary widely. Since their unregulated, the hedge fund manager has nearly carte blanche to do whatever they see fit.

Some hedge funds use long-short strategies. They may buy securities long, holding them for a period of time hoping they’ll appreciate in value. They may also sell securities short, borrowing securities to sell them at current prices, hoping they’ll drop in value so they can be repurchased later at a lower price.

Other hedge funds use derivative strategies. Derivatives are investment contracts which get their value from some other underlying security. Derivatives are more commonly known as options and futures contracts. Derivatives typically use a great deal of leverage and can be incredibly risk!

What’s wrong with hedge funds?

Liquidity. Unlike mutual funds and most other investments, hedge funds aren’t very liquid. Hedge fund managers use very specific trading techniques. Those tactics don’t always have liquidity. Since the investments aren’t very liquid, investors should know their money can be tied up with limited liquidity for a certain period of time called the “lockup period”.

Compensation. Another big difference between mutual funds and hedge funds is how the fund manager is paid. Hedge fund managers receive a percentage of the returns they earn for investors. They also earn a management fee.

Hedge fund fees are substantially higher than mutual fund fees. A typical compensation structure is 2% of the investment and 20% of the profits they generate for the investor.

This may sound like a great deal! 2% of your investment and 20% of your profits for an “ultra sophisticated high end fancy shmancy investment”. It also encourages the hedge fund manager to be VERY aggressive with your money. They are getting 20% of your profits after all!

Inaccessible. Because they’re very risky hedge funds also aren’t available to the general public like mutual funds. Hedge funds are available only to “accredited investors”. An accredited investor must have income of $200,000 per year for the last two years (or $300,000 for married couples) and a net worth of $1,000,000+ (not including their home). You have to be pretty well-off financially to even have access to invest in a hedge fund.

Should I invest in a hedge fund?

So hedge funds are really aggressive, highly illiquid, hard to understand, the manager can do whatever they want with your investment, and only open to “accredited investors”… they must have AMAZING PERFORMANCE RIGHT?

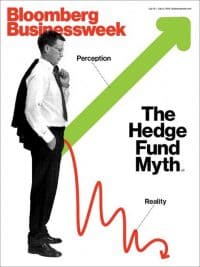

Not so fast! In the article I mentioned above I eluded to the fact that hedge fund performance wasn’t so hot. Take a look at the article and you’ll see what I mean. Here’s the low-down:

- Due to performance reporting biases, their actual returns since 1996 are about half as good as they report (actual 6.3%, reported 12.6%). This is largely due to survivorship bias I suspect (meaning many go defunct so their bad performance isn’t carried forward to compete against remaining funds, hence only the decent performers survive).

- Volatility is higher

- Maximum drawdowns are worse (the total drop from top to bottom of a loss)

The report states that hedge funds voluntarily report results to the databases. If you have a crummy hedge fund, what’s the chance you’re going to publish how crummy you are? You probably won’t get new investors for your next big flop!

The report goes on to state that hedge funds haven’t outperformed traditional investments of stocks and bonds. After you remove the reporting biases they do not routinely generate double digit returns.

The next time your neighbor tells you about his hot new hedge fund, just wink and wish him well! Chances are very good you’ll be outperforming him with your globally diversified and balanced portfolio of stocks and bonds owned through simple mutual funds!