Here Are 13 Things You Need To Know Before Investing

If you’re thinking of investing in structured notes you need to educate yourself! In this webinar I discuss the risks of structured notes and the benefits, including two examples of a Goldman Sachs structured note and a Barclays structured note.

Educate and enjoy!

WHAT IS A STRUCTURED NOTE?

A structured note is a debt obligation typically issued by one of the large investment banks. The debt obligation—or “note”—is paired with a series of derivative investments designed to accomplish certain financial objectives if certain market events are reached or avoided.

Each structured note has a finite maturity date (however some may be called prior to maturity) and is subject to the credit of the issuer. They’re similar to any other corporate bond offering, however, there are some bells and whistles attached to them. It’s the bells and whistles that can make investing in structured notes attractive when used properly.

Structured notes are considered a “hybrid security” because they’re not a “traditional” investment like stocks or bonds. Rather, structured notes have characteristics of both bonds and stocks.

Several of the large investment banks create and issue structured notes. Some of the major offerings you may find are:

- Goldman Sachs structured notes

- Credit Suisse structured notes

- HSBC structured notes

- Barclays structured notes

- JP Morgan structured notes

- Fidelity structured notes

- And several others . . .

It’s important to note that each bank issuing a structured note will have different pricing. Goldman Sachs structured notes may price attractively for a certain set of bells and whistles, yet JP Morgan structured notes may price better for a different set of bells and whistles. This makes price shopping structured notes critically important for the investor.

STRUCTURED NOTES USE DERIVATIVE SECURITIES TO CREATE THE “BELLS AND WHISTLES”

A derivative security is simply something which derives its value based on something else. Common examples of derivatives which are used in structured notes are call options and put options.

A call option gives the investor the right to buy a security at a specified price within a specified period of time. It’s similar to a lease option on a house where the investor has the right to purchase the home at a certain price by a certain date. The investor may or may not exercise that right.

A put option gives the investor the right to sell a security at a specific price within a specified period of time. These types of put option contracts have been used for centuries to protect the value of a farmers crop for example. The farmer may sell the right to buy his crops at a certain price which may limit his upside if the crops are good, but they limit his downside as well by taking the premium paid to offset his risk the crops are poor.

Call and put options are bought and sold to accomplish certain financial objectives, such as reducing investment risk or leveraging investment returns. It’s these types of derivatives that are constructed in a meticulous fashion to accomplish certain monetary outcomes if certain conditions are met or not met.

What can structured notes do?

The financial outcomes associated with structured notes are based on an index, interest rates, currencies or a security’s performance (such as the S&P 500, the Euro, or AT&T stock). They can be structured to:

- Provide downside market protection

- Provide upside market participation with or without leverage.

- Provide a stated payment at maturity if certain market conditions are met or avoided.

- Provide certain interest payments at various points in time if certain conditions are met or avoided.

- And just about anything you can imagine from there!

What types of structured notes are there?

There are several types of structured notes available. These are just a few of them for reference:

- Principal protected notes are similar to a fixed income asset designed to protect the investors principal regardless of the performance of the underlying asset.

- Buffered notes provide some downside protection. For example, if the S&P 500 is down 10% you’ll get your principal returned, and if it is down farther you’ll only lose 1% for each additional 1% of loss turning an 18% loss into an 8% loss.

- Return enhanced notes provide some form of leverage to returns on the upside. For example, if the S&P 500 is positive 20% in 4 years and you have 1.5 times leverage, your actual return would be 30%—far better than the 20% even after you count the roughly 7% of lost dividends (which I’ll discuss later in this article)!

- Market-linked CDs (Certificates of Deposit) provide FDIC insurance up to applicable amounts as well as potentially enhanced performance based on an asset class or underlying index. That performance is typically limited by participation rates and/or caps.

HOW DO STRUCTURED NOTES WORK?

A structured note has both a bond component and a derivative component. The bond component is used to provide principal protection and the derivative component is designed to accomplish certain objectives—the “bells and whistles”—when conditions are met or avoided.

Let’s assume the investor purchases a 5 year note for $1,000:

- The bank will issue a zero coupon bond. Let’s assume they get $825 out of every $1,000 for a 5-year note. This means the bond will mature at par—$1,000—which equates to roughly a 4% annualized return. The issuing bank can use this money for whatever they want to, it’s effectively the same as any other corporate bond issue.

- The bank then takes the remaining (roughly) $175 and creates a derivatives package designed to accomplish certain financial goals. They may buy options, sell them, or any combination therein.

- I mentioned “roughly $175” because there are additional fees to create the legal document for the structured note and bank fees embedded. There also may be brokerage commissions which substantially reduce the note’s financial benefits. It’s important to note Redrock Wealth Management NEVER ACCEPTS ANY FORM OF COMMISSION OR KICK-BACK, hence our notes are designed without any embedded commissions thereby increasing the notes potential performance.

STRUCTURED NOTES HAVE DIFFERENT FEATURES

Structured notes have several different features to be aware of. Some of these are:

- Auto-call where the note will be “called” from you (meaning the issuer pays you what they owe you) if certain conditions are met or avoided.

- Callable notes give the issuer the right to call the note from you at their desire, typically if conditions are favorable for them to do so (such as refinancing the debt component at a lower rate). Typically there’s a minimum time a note can be called that must be met after which they’re callable at certain periods in time.

- Capped structured notes can limit your upside. Some structured notes have “Caps” which means the upside return is limited at some point. This brings in the risk of having a market outperform the Cap and you’re left with lower returns and loss of dividends over the timeframe.

- Participation rates can vary and you need to be aware of what they are. For example, 80% participation means you’ll only earn 80% of the underlying index (and don’t forget you’ve given up the dividend income).

- Leveraged notes can provide you higher returns than an underlying index or security. For example, you can structure a note to provide twice the return of the S&P 500 if certain conditions are met.

WHAT ARE THE FEES OR COMMISSIONS TO INVEST IN A STRUCTURED NOTE?

As a fee-only fiduciary advisor, we never accept any commissions, kickbacks, perks, trips or benefits whatsoever. We design structured notes with no additional compensation for us as the financial advisor. That being said, most structured notes are sold with embedded commissions which reduce your investment performance substantially.

Many investors suspect there’s “something on the back end” for us, however, this can’t be further from the truth. In contrast, it’s a great deal of extra work to create and manage the structured note process to which we don’t receive any additional compensation. What we do receive is the satisfaction that we’re doing everything we can to improve our client investment returns and financial plan results (even if by modest amounts.)

That being said, most other “brokers” (who masquerade as financial advisors) do indeed reap large commissions to sell these investment products. Their commissions are “baked into the cake” and the average investor will never know what they paid to the broker or their firm for that structured note. Some commission structures range from 3% to 5% or more!

Bank and note shopping/creation fees for our structured notes are typically .25 to .50 per year and are deducted from the initial investment. For example, a 4-year structured note would have internal fees of 1% to 2% in total. These fees are similar to a low-cost mutual fund on an annual basis.

WHAT ARE THE STRUCTURED NOTES RISKS?

Creditor risk is the primary concern. Should the issuing bank go out of business the note could be worthless as with any other corporate bond regardless of whether the underlying investments have a positive return or not. A notable example of this is Lehman Brothers which filed for bankruptcy on September 15th of 2008 (middle of The Great Recession). Had you owned a Lehman Brothers structured note at the time it became worthless.

Market risk is also a major concern. While some notes have buffers and other protection factors built in to reduce the impact of a bad market, you may still suffer a financial loss as with any other investment that’s not FDIC insured or principal protected.

Liquidity risk is another concern. Should you need access to the investment in a structured note prior to maturity you’ll be forced to sell on the open market. There may or may not be buyers willing to invest in your note, however, there is generally always some buyer willing to purchase it at some price, typically a discount to what it’s really worth financially.

Pricing anomalies exist as well. As with any other bond or stock investment it’s only worth what someone will pay for it on any given day. While there are services that look at the underlying structure of the note and provide an estimated price, it’s only an estimate and sometimes the pricing may vary substantially from what it’s really worth as a financial asset. Our custodian TD Ameritrade uses a company called ICE Data Services to price the structured notes we use daily.

Call risk or prepayment risk means the issuer may redeem your note before it matures in which case you may not get the full financial value as if it were held to maturity.

Exchange rate risk exists for structured notes involving any foreign currencies. This isn’t unusual as many mutual funds experience the same exchange rate risk.

The fees and commissions can be absolutely outrageous on broker-sold structured notes with massive commissions lining the pockets of slick salespeople. Not every structured note has outrageous fees and commissions however, but the majority of them do.

DO I GET THE DIVIDENDS FROM THE INDEX UNDERLYING ASSET?

No, unfortunately. You don’t get any of the dividends when you own a structured note. For this reason, it’s critical to make sure you include the loss of dividend income in your structured note analysis to make sure it still makes sense even without the dividends.

HOW ARE STRUCTURED NOTES TAXED?

Always consult your tax professional for accurate information on structured note taxes. Generally speaking:

- Principal protected notes and those which are designed for current income will be taxed at ordinary income tax rates. They may also be subject to phantom gain taxes each year prior to maturity.

- Notes without current income (assuming a maturity of longer than 12 months) are taxed at long term capital gain rates.

ARE STRUCTURED NOTES A GOOD INVESTMENT? WHAT ARE THE BENEFITS ANYWAY?

Structured notes can be a good investment under the right circumstances and provided you’re well aware of all of the risks involved. Some of the ways structured notes are good are:

- Creating and targeting a more predictable—more narrow—range of expected returns.

- Diversification. It’s a different type of security from the typical stock and bond mutual funds and ETF’s.

- Hedging or downside protection/reduction can be a component of structured notes. This may allow otherwise conservative investors a more palatable way to enter an otherwise volatile investment asset class.

- Customized income payouts. You can find a structured note which may provide unique payout timing more suitable to your needs.

- Potentially higher investment returns with little to no risk. This can be accomplished through downside protection components or principal protection features.

- Potentially higher investment returns in a sideways market. Structured notes can provide a great investment return in a sideways—or flat—market if they’re set up properly.

- Potentially higher yields when returns are low.

- Use of leverage to generate potentially higher investment returns.

- Structured notes are a great option for a defined benefit or cash balance plans due to the long term nature of such plans and narrow range of required investment returns.

HOW DO STRUCTURED NOTES FIT INTO AN OTHERWISE DIVERSIFIED AND WELL-BALANCED PORTFOLIO?

How much to invest in structured notes

First off, risk only what you can afford to risk! Since the biggest risk you face (in my opinion) is the credit risk of the issuer it’s critical to keep that risk tolerable.

For most investors, 5% to 15% of their entire portfolio is a reasonable allocation to invest in structured notes. But it doesn’t stop there!

That 5% to 15% should also be limited by asset class, meaning 10% is a reasonable guideline for how much of your stock allocation can be in structured notes. Taking a deeper dive, 10% is a reasonable guideline for how much of your international stock allocation could be in structured notes.

5% to 15% of your overall portfolio is only a starting point. Each asset class should have its own limitations—or targets—for structured notes.

While many financial advisors use only the starting point of 5% to 15% of the overall portfolio, this can lead an investor down a risky path. Say for example you are only investing in structured notes tied to US stock indexes. This means you’ll be replacing too much of your US stock investment with structured notes!

For example, if you have a 1 million dollar portfolio and you’re a 60% stock and 40% bond investor with a 60/40 US to international split, using 15% of the overall portfolio means that over 41% of your US stock allocation could be in structured notes (150k/600K*.6)).

I don’t want 40%+ of any major asset class tied up in structured notes! For this reason, it’s important to look at multiple indices and slowly layer into each one, replacing only the asset class your structured notes underlying performance comes from.

Layer structured notes into your portfolio over time

Layered entry points are critical. Implementing structured notes over time provides high and low and average points of market performance to layer into. These layered entry points should provide a higher degree of performance overall as you pick different strategies for different periods of market performance.

For example, if we were currently in a real estate bear market and had suffered substantial losses for a period of time, why not consider a structured note tied to a real estate investment trust index with minimal to no downside protection and leveraged performance on the upside? You’ve already endured lengthy and substantial losses, take a portion of your portfolio and use some leverage for the eventual index return to normalcy (which may easily take years to appear keep in mind).

Or if the international stock market had a massive run-up for a period of time, why not consider a structured note that would provide substantial downside protection but limit your upside? You’ve already enjoyed the big gains, is narrowing in your range of investment returns and limiting your downside using structured notes so horrible?

Diversify your issuers for credit diversification

Diversified issuers for credit diversification is also key and goes hand-in-hand with layering in your entry points. If you’ve got credit risk/exposure to Goldman Sachs through a structured note, why not look at JP Morgan structured notes or Morgan Stanley structured notes for the next one?

By diversifying the issuers, if one of them happens to run into a 2008 scenario all over again and goes belly-up, it’s possible the other issuers will be fine. I would never recommend putting all of your structured notes with one issuing bank for credit diversification reasons.

Enhance your returns with structured notes

Can we beat the projections using a structured note strategy? I believe financial planning—especially with retirement—is more important than the investment strategy used or investment vehicles that were chosen.

In your retirement plan, you must incorporate a set of basic capital market assumptions. For example, we assume today that US large cap stocks will return roughly 6.5% per year over the next five years. That’s based the professional analysis and software we use for planning.

If we can structure a note that gives us an 85% chance of achieving 7% per year with some downside protection it may be a good fit for the retirement plan. We’re not only giving investors a high likelihood of OUTperforming the US stock market projection, but we’re adding in some downside protection “just in case”.

Even small amounts of outperformance over long periods of time can really add up!

Structured notes maturity

Structured notes should typically be long enough to have a reasonable likelihood of hitting the objectives tied to them. What I mean by this is there’s no telling what direction the US market is going in 5 months, but the statistics bear out that in 5 years it’s likely to be higher than today (not always, but it’s fairly likely).

Notes should range in length from 3 to 6 years in my opinion, and I’d only use the shorter end of that range if there was a major reason to do so such as a prolonged bear or bull market where the statistics show a high likelihood of a reversal (or reversion to the mean).

TWO STRUCTURED NOTES EXAMPLES

Goldman Sachs Structured Notes: Euro Stoxx 50

This is a structured note we created in late 2018. As you may remember the stock market, in general, was seemingly in a tailspin at that point in time. More specifically, international stocks were in worse shape than we were here in the US.

Our projections for the international stock market at that point in time was somewhere around 7% to 7.5% per year. I can’t remember exactly what it was as projections change each year and we recently updated our numbers to reflect the current market environment.

The underlying index for the Goldman Sach structured note is the Euro Stoxx 50. That index is similar to the Dow Jones Industrial Average for our US markets in that it’s a group of the large blue-chip type of companies.

The Euro Stoxx 50 had dropped from about 3,600 to the 3,100 range when I started creating that structure—a loss of about 14% from January 1st to mid-November. With our international stock market projections being in the low 7% range the goal was to improve that performance with a structured note . . . even if by modest amounts.

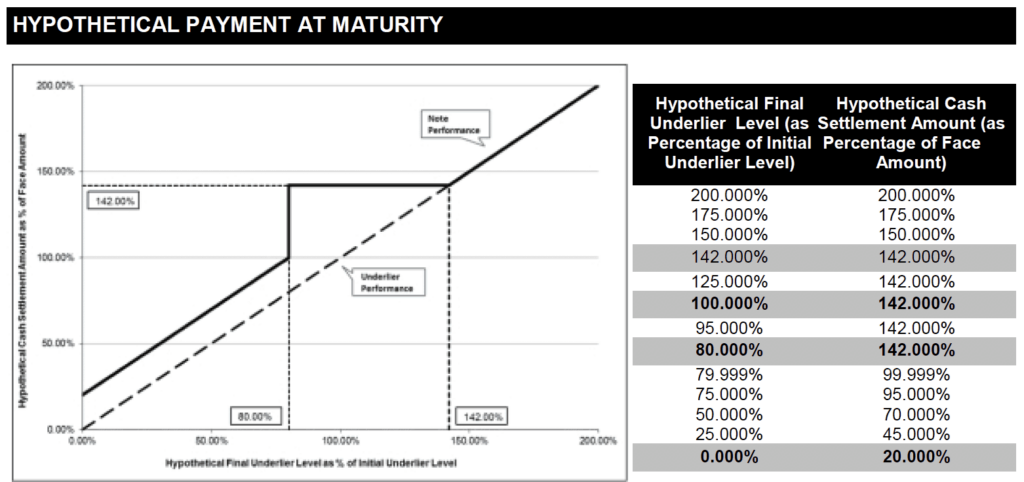

Here’s how the Goldman Sachs structured note on the Euro Stoxx works:

Click on the image above for a large version. This is a digital note, meaning there’s a range of returns in which the payout is going to be fixed no matter where the ending index—in this case the Euro Stoxx 50—ends provided it’s within the allowable limits. The allowable limits in this situation are -20% to +42%.

Assuming the Euro Stoxx 50 is NO WORSE THAN -20%, investors will get a final payment in December of 2023 of at least 42%. That sounds too good to be true right? The index could actually be DOWN by 20% and the investment return is +42%!

Even better if the index is ABOVE 42% the investor gets whatever the investment returns. So if the index on December 19th of 2023 is +50%, the investor gets a final payout of their original principal plus half (better than 42%)!

Even better than that is if the index is WORSE than a loss of 20%, the investor only loses a point for point below that watermark. For example, if the Euro Stoxx 50 is down 30%, the investment return is -10% for the 5-year timeframe.

Remember the risks associated with Goldman Sach structured notes and ALL structured notes for that matter! The looming risk is Goldman Sachs going out of business and not paying the note off which could happen as we’ve seen with the Great Recession of 2008.

In that situation however, the overall stock market was down 40% or more depending on what points you pick to measure it and what indexes you measure. I’d argue your initial investment of let’s say $10,000 would only be worth 60% or so anyway if you stayed in the actual index mutual fund (not invested in the structured note.) So your real-life loss wouldn’t be the full principal investment, but rather the actual value of the indexes at that point MINUS zero meaning if market conditions sent your index mutual fund value plummeting you would have incurred a loss of some significance anyway.

Barclays structured notes: Worst of S&P and Dow Jones Industrial Average

As of this writing this note is being created and allocated to client accounts. After many iterations I’ve reviewed and analyzed in great detail, I’ve settled on this structure:

- Underlying indexes are the Dow Jones Industrial Average and the S&P 500

- The WORST performing index is the one used in the final calculations

- It’s a 4 year term

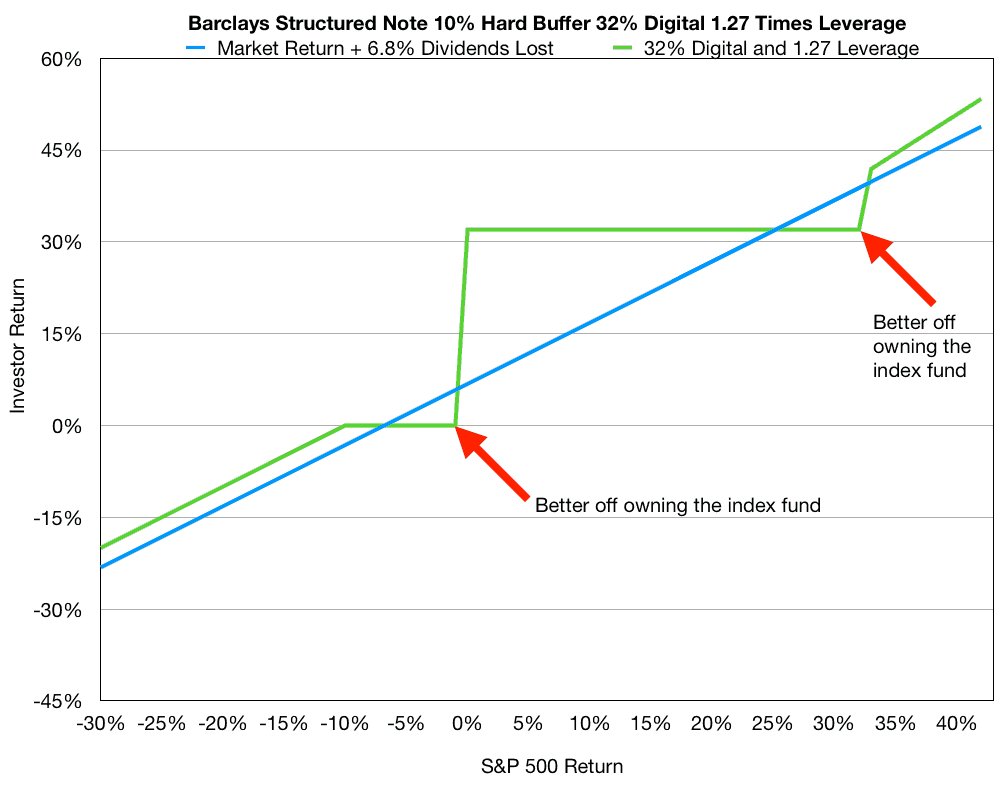

- Should the index be flat to +32% the investment return is +32% or about 8% per year (not exactly 8% if you included compounding returns, but close)

- This is a 1.27 times leveraged structured note as well for returns OVER 32% meaning, if the worst of the Dow and S&P500 is +32% the investment payout is 40.64% (32% X 1.27)

- Should the worst of the two indexes be anything negative to -10% the investment returns the full principal amount but nothing additional

- Should the worst investment return of the two indexes be anyting worse than -10% the investment loses point for point thereafter, so if the Dow is -13% and the S&P 500 is -15% the investment loses 5% in total

Considering the US stock market is in striking distance from all-time highs, this Barclays structured note provides some downside protection but a nice investment return if the indexes linger around for 4 years doing not much of anything in the process. That return is 32% (assuming it prices the same when it closes) or about 8% per year (again, the annualized return will be less if you considered compounding).

On the upside, if the worst of the two indexes is 32% or more the investment returns 1.27 times whatever that performance is. This makes the possibility of earning about 10% per year very reasonable looking at historical performance of the S&P 500.

Why create a note which uses two indexes? You get better pricing simply. There are more moving parts so it’s tougher to hit the parameters of the note. That being said the correlation of the S&P 500 to the Dow Jones Industrial Average is well into the 90% range depending on how you’re calculating it, so the results for the two indexes should be similar at worst.

Similar performance and a high correlation don’t mean it’s foolproof, the two indexes can still deviate substantially over 4 years. It’s the little things like that you must keep in mind when investing in structured notes.

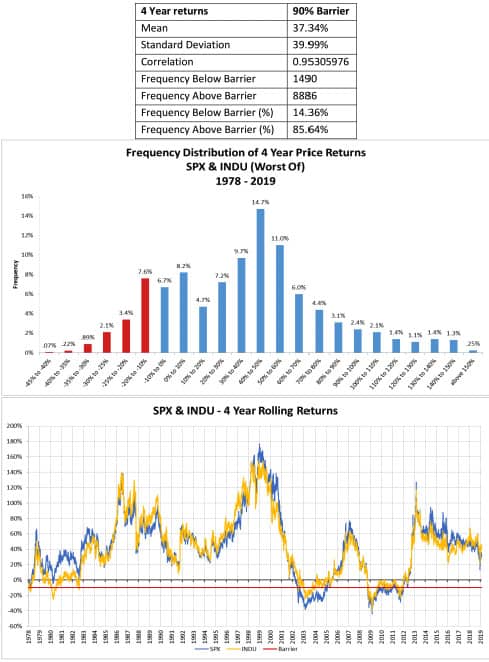

I don’t have the offering document on this note yet as it’s in the process right now. That being said I do have some backtesting results:

As you can see the correlation of the S&P 500 and the Dow Jones Industrial Average is very high. While they’re not the same, they’re very similar.

If we achieve the historical mean return of 37.34% (noted on the chart above) we’ll earn 1.27 times leverage on that, equating to a 47% return. I’m IN NO WAY predicting that will be the result, I’m just illustrating the backtesting of this concept and the potential returns by looking at historical returns.

85.64% of the time the worst performing index was better than -10% and the investor at least got his investment returned (again keeping in mind the risk factors above, specifically credit default).

Doing the math on the chart above:

- 14.4% of the time the worst performing index will be worse than -10%, meaning you’ll have a loss (but only point for point worse than -10%)

- 6.7% of the time the worst performing index is between 0% and -10%

- 20.1% of the time the worst performing index will be from 0% to +30% in which case the payout would be 32% no matter where in between it falls

- 58.8% of the time the worst performing index will be greater than +30% (remember it must be greater than 32% to get the leverage of 1.27 times)

Visually, it looks like this:

Please note: The above chart I created is only a hypothetical example illustrating various investor returns for the corresponding market returns.

To make this a “fair fight”—well more accurately for valuable analysis—I took the dividends forfeited from our US equity index fund and added them to the market return above. Those amounted to about 6.8% over the 4-year timeframe. That gives us an apple to apple comparison on this particular structured note concept.

Even though I’ve accounted for the dividends lost, the only two potential scenarios are the small triangles noted by the red arrows. In those two cases, you would have been better off owning the actual index fund and not the structured note.

In case you’re curious, I backtested this using 4-year rolling S&P 500 returns going back to 1929 and over 90% of the actual returns WERE NOT in the two triangles! Keep in mind backtesting with the Dow incorporated would change the results but not significantly.

WHERE CAN YOU INVEST IN STRUCTURED NOTES

Structured notes are widely available through most investment custodians. You can invest in structured notes through Charles Schwab, Fidelity, or TD Ameritrade for example.

The big investment banks will typically sell you THEIR structured note offerings versus shopping for the best pricing and availability across all the investment banks. For this reason, you may or may not get the best possible bells and whistles as this can quickly become a proprietary investment product.

Incapital is a company which produces and promotes structured notes. You can search their website to find several currently available structures to consider, however you’ll need to use an investment custodian or broker-dealer to actually purchase structured notes.

STRUCTURED NOTES GET A BAD RAP!

Structured notes get a bad rap!

The SEC has focused on bad broker (not advisor) practices which happened to include flipping structured notes. Wells Fargo paid 5 million because their brokers were coercing structured note investors to liquidate prior to maturity and “flip” the money into new structured notes for a new set of fees and commissions. This is completely dishonest and unethical at best and in my opinion a criminal practice.

Lehman Brothers pitched many of their structured notes as principal protected—which they actually were—but subject to the credit of Lehman Brothers. When Lehman Brothers collapsed in late 2008 the structured notes became worthless. Since they were pitched as “principal protected” many investors were unaware they could lose all of their investment.

Structured notes are often misrepresented and misunderstood. Advisor Perspectives for example laments over one particular structured note designed for a seemingly excessively high yield for 10 years when in fact it’s unlikely that the note would deliver as expected for several reasons. This doesn’t itself make all structured notes bad per se, however it does highlight the fact that someone investing in structured notes really needs to understand the nuances of them and it’s critical they do their homework.

STRUCTURED NOTES IN SUMMARY

Structured notes are growing more and more popular and many financial advisors are using them wisely to create more predictable ranges of investment returns.

The SEC is monitoring sales of broker sold structured notes to help protect the public from making an uninformed decision on a highly complex investment vehicle.

Structured notes should only be a part of a well-diversified low-cost investment portfolio, and typically in a small amount such as 5% – 15% of the overall portfolio with roughly 10% of any individual asset class as a general guideline.

When used properly and methodically structured notes can add a great deal of value to your investment plan and portfolio. The key is not looking at them individually as an investment per se, but rather layering them into an otherwise well constructed and diversified portfolio.

Practical and helpful.Thanks

Glad you enjoyed the information! Investing in structured notes isn’t for the faint of heart. You really need to know what you’re doing and have a balanced investment portfolio.

Hi, is the payoff mainly coming from shorting option premium and anything else? thanks!

Structured notes are far too complex and diverse to say the payoff comes mainly from any one strategy. It varies widely.