This video and blog post was a part of my Wealth Summit series of interviews. Enjoy!

Greg: Hello Wealth Masters. My name is Greg Phelps. And I am your host to the Wealth Summit.

The mission here at the Summit is simple. We want to educate and empower you with actionable tools, tips, and takes to help you grow, protect, and maximize your personal wealth.

Today’s guest Mark Maurer is going to talk about long-term care insurance and so we are going to focus today on that protection factor of the mission statement. So Mark, are you ready to help us Master our wealth?

Mark: I am ready.

Greg: All right, great!

So a little bit about Mark. Mark assumed the reins of LLIS which stands for Low Load Life Insurance in 2012 after nine years of learning the family business. He’s built upon the foundation that Judith, his mother, had built by adding more talented staff members and new technology.

He’s happily married. His wife Leah is an adjunct mathematics professor at the University of Tampa. He also has two children. He’s got a nine-year-old son, Jay, who’s into soccer and any book on sports, and a seven-year-old daughter, Marie, who loves ballet with our own Miss Ashley and art.

What most people don’t see him do is work out. Mark’s at the YMCA at the crack of dawn before the sun is even up when most people are still sleeping. Mark, today I can tie you because I was up at 4 a.m and ran six miles. So we’ve got something in common just today only.

Mark: You, you win because I slept in today.

Greg: Oh, no.

Mark: You win and with the time change you won by like seven hours or so.

Greg: All right, I’m gonna chalk that up to just a small victory for me today Mark. So that’s a little bit about your bio. Go ahead. Take just a quick second, fill in any gaps that you might want to share with the Wealth Masters.

Mark: Sure. No, you know, I’d grown up hearing about insurance, learning about it, but I went away to school, I worked for an international shipping company for a number of years.

I worked for a natural gas Trader in Gainesville, Florida and one day, sort of had a conversation with Judith about being the succession plan, and I think I’d never really thought about doing it.

So I got to experience a lot of different things. It wasn’t ever assumed that I’d be here and I love it. It’s been years being here. And I really enjoy doing what I do.

Every day is like a puzzle working with financial advisors who say and my clients have this, here’s what I’d like them to have. How do we rework, adjust, change?

Greg: Improve.

Mark: That’s fun for me to—improve— that’s fun for me to do every day!

Greg: Well just for the viewers out there, I met Mark through our organization that we both are involved with which is NAPFA, the National Association of Personal Financial Advisors. Goodness, gracious. Actually. I just looked at my original life policy I got from you back in 2008. I pulled that up yesterday, which was probably the best investment even though I hopefully will never pay off . . . the best investment that I’ll ever have made.

So anyway, we’re both associated with the National Association of Personal Financial Advisors, which is a group of fee-only fiduciary financial planners. So make sure you remember those terms, fee-only fiduciary when you’re working with a financial advisor.

So Mark, let’s go ahead and kind of dig right in because when I approached you to be a speaker at the Wealth Summit, I am not an expert in insurance–I am a CLU but I’m by far from an expert in insurance–and I get these questions from clients and they come in and they say hey, you know what If I get sick late in life? So let’s just go ahead and start with a very very foundational level and talk about “What exactly is long term care insurance?”

1. What is long term care insurance?

Mark: Sure, and long-term. Take a step back. If we think of health insurance, what does health insurance do?

Well, health insurance doesn’t prevent us from getting sick. Health insurance is a funding mechanism to pay for things if we do get sick.

Long-term care insurance is sort of the same thing. When a long-term care insurance policy would provide benefits is IF someone becomes cognitively impaired, they’re diagnosed with Alzheimer’s, they need hands-on or standby assistance to do activities of daily living such as toileting, transferring, eating, bathing.

So they’re all things that at some point in life, we may not be able to take care of ourselves as we hoped. And the other part about long-term care is again, unlike medical insurance that’s usually used for prescriptions, doctors, and things that are designed to treat and get you better. Long-term care is sort of you know, the name of it gives it away long.

It’s for something that’s chronic, that probably isn’t going to get better. And so you have those two different things, health insurance, Medicare for treating specific things and then long-term care that comes into or long-term care insurance that comes into effect when I’m not going to necessarily get better from these things.

Again Alzheimer’s is something I think that’s touched a lot of people through their families, somebody they know and that’s a really good, you know idea you hope one day we have treatments for Alzheimer’s, hopefully, one day we have a cure, a medicine that can cure it today.

It’s all about, you know, once you-you’re diagnosed with it or have that as a concern then how do we fund people to care for Mom, Dad, Grandma, Grandpa and where are they going to get that care. And so the long-term care insurance is the funding mechanism or vehicle behind that, to be able to provide care.

Greg: Okay, and you know really quickly and off the slide topic, I guess, if we don’t plan for things like long-term care expenses later in life what happens if there are just no assets there to take care of somebody who needs years of care, what happens?

What happens if I can’t pay for long term care?

Mark: And that’s a good . . . that’s a good question! Good point because if you don’t plan you’ve decided, you know, that’s your default plan is to do nothing. And so then you’re relying on usually the government which people are surprised that Medicare really doesn’t cover much for long-term care.

Medicare may provide benefits for only up to a hundred days. Like I said before, Medicare health insurance is designed for things that get you better and then get you off claim or benefits.

So Medicare usually covers up to a hundred days of long-term care. After that, if you really truly have no assets that Medicaid may be able to cover some of those expenses. One of the problems with Medicaid is that you may not get to pick where you receive care.

Most facilities are either Medicaid eligible or may have a few Medicaid-eligible rooms or spaces. And if you want to be close to home, you may not have that option with Medicaid.

Your other option is family. You see, family members may be able to provide that care. There’s a lot of people who are living with their children and the children are their long-term care plan and you know again you need to make sure that if your children are your long-term care plan that they know about that because you know, that may not be what they were planning on.

Greg: Right. Okay, so you’re really kind of subject to the whims of maybe I get a little bit of coverage from Medicare and then maybe some coverage for Medicaid, but it’s completely out of my hands. I could end up in you know, 50 miles away from my family.

Mark: Exactly.

Greg: Yeah, or you end up living with your kid.

Mark: And those are the yeah when you haven’t planned for something either by having enough assets, enough income, long-term care insurance, whatever it might be–those tend to be the default or fall back of what happens?

Greg: Okay, and what do we have something like 10,000 people turning baby boomer age and you know every day or not baby boomer age, but retiring.

10,000 baby boomers retiring every day. This is an aging population. So it’s just a really critical issue.

Mark: Right. And it’s you’re seeing a lot more to your point of everybody retiring, and you’re seeing more and more multi-generational households than ever before because Mom and Dad were relying mostly on Social Security and that was going to be how they were going to pay for everything.

And the cost of needing care far exceeds what a normal income might be, an extra fifty-sixty thousand dollars a year if you need substantial care. And so where does that come from? Whose pockets is that coming from?

It can be the government’s, it could be the kids taking care of Mom and Dad. One of the things we also look at with long-term care insurance has a lot of people, one of their primary assets is their home.

That may have hundreds of thousands of dollars of equity, but if somebody needed to pay a nursing home, how do you fund that? You may want to leave the house to the kids and so long-term care policy, right. You have to sell it.

Most people think that’s a conversation I would never want to have. Most people probably go into a facility, don’t want to sell the house because they don’t want to admit —you know— I’m probably not coming home. And so you have this large asset maybe not a whole lot of spendable assets and long-term care insurance helps be that. I can use this to pay for care leaving the house that I can pass to the kids.

Greg: Well, I can definitely speak anecdotally. I think there’s a big piece of mind factor that comes with planning for this upfront.

I know in our family, and I don’t mind sharing personally, you know my stepdad has later stages of Parkinson’s and so we’re in the initial stages of, kind of figuring out “Hey, when do you start looking at using this long-term care money and so forth . . . and how does that play into the overall picture?”

So it’s a really important discussion to have with your family, your spouse, and people that are close to you, but what I’d like to kind of talk about now–and Mark just so you know this slide will stay up for a little bit–I’d like to talk about what exactly are long-term care costs, roughly?

Now I know you pulled this quote for Nevada because that’s where I’m located in. Thank you. And so that obviously is going to vary state by state but just kind of run through some of these things.

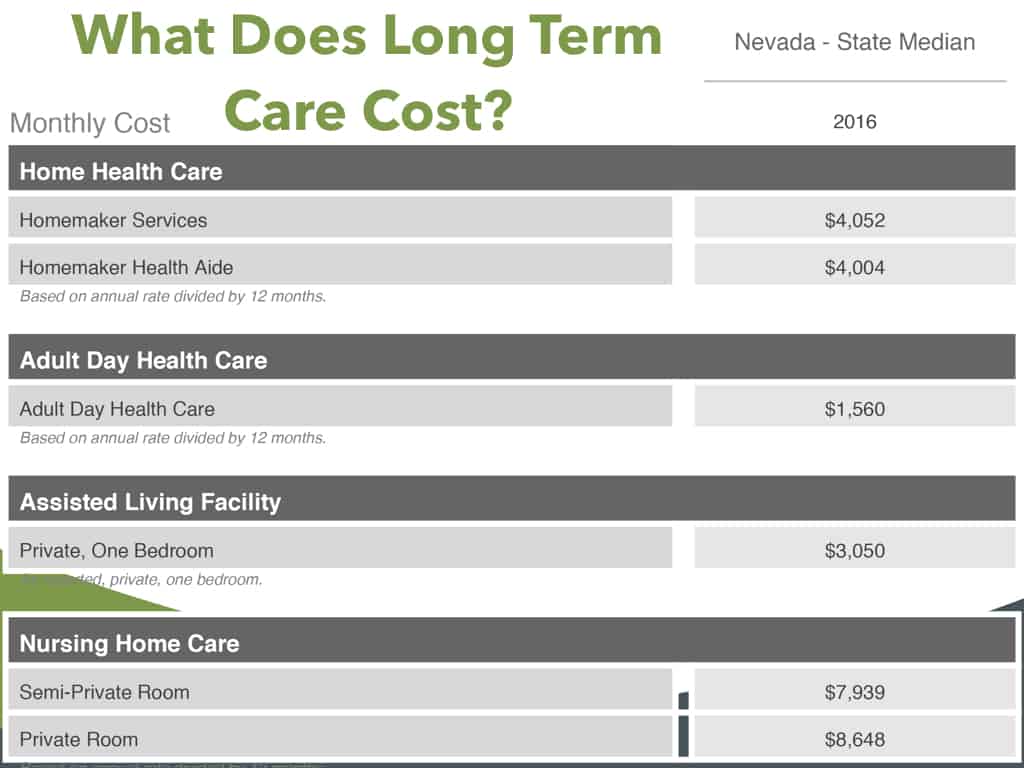

2. What does long term care cost?

Mark: Sure and so we have the slide there and Genworth does a study every year and they survey thousands of providers all over the country to to to get these estimates and it’s usually broken down into two. I think there are four different subsections.

Home health care

So you have your home health care. A long-term care insurance policy once you meet those triggers of either having cognitive impairment or needing help with two of those activities of daily living, and you need what they call a hands-on or standby assistance to do those, then you’re eligible for benefits.

The long-term care policy is usually defined as $3,000 a month. You can use that for different levels of care. And then where you receive the care is up to how significant, let’s say, the condition is.

So one of the places that you can receive benefits is in your home and the slide is showing that monthly in, Nevada on average, and I think it was Yogi Berra who said if you put one foot in a bucket of boiling water and one foot in a bucket of ice water on average you’re comfortable.

So this is—you know— designed to be just a really ballpark number, but it says that around on average about four thousand dollars a month is what somebody can expect for homemaker or home health care services. So this is usually for somebody to come in about eight hours a day to help care for somebody whether that you know it is helping them get bathed, probably doing a little bit of helping with meals, that’s about four thousand dollars a month on average extra.

So —you know— that’s not including food. All of your normal living expenses are built in there. That’s an additional 48 thousand dollars a year if you just need care in the home.

Adult daycare

There’s a second subset. That’s the Adult Day Care and this would be probably for somebody who’s living at home or living with her children and they still need to work.

They’re probably in their 40s and 50s. The Mid 50s, you know, they’re in their primary income-earning years and are caring for Mom and Dad, but they have to work, they can’t be home all day so there’s Adult Day Care Facilities where you basically it’s not unlike child daycare. You take your parents to this facility.

They help them and watch them all day. And then you pick them up at the end of the day. And so and that’s quite a bit less because it’s a facility.

There’s usually more home health aide, you figure one on one. Adult Day Care can be one provider, one care caregiver for multiple people and that’s about $1,500 a month.

Assisted living facility

You have your assisted living facility. This is my growing up in Tampa. Our grandparents didn’t, our grandparents were in Nebraska and we moved to Florida when I was in third grade and across the street, we had neighbors who were grandparent age and we called them Grandma and Grandpa Demery and you know, they were like our grandparents and at some point my grandpa Demery passed away.

My grandma Demery moved into an assisted living facility. She didn’t have Alzheimers, no cognitive impairment. She was just older and little and frail and just things were hard.

And so she was in an assisted living facility and the cost of that for private one-bedroom was $3,000 a month and that’s not usually considering some things like food.

Being here in Florida. We have some great assisted living facilities. I can’t wait till one day —you know— like I want to move in today. They have a Starbucks in the basement, you can get smoothies anytime you want. Oh, yeah big-screen TVs with movies at night.

This is where I’m going, but they don’t let me in so it’ll but those are facilities that are about another $3,000 a month for that sort of level of care.

And those are probably the last study I read, about seventy percent of people who are receiving long-term care fall into one of those three. These are the most common.

A lot of people don’t necessarily move into that last category the nursing home care sort of until the later stages and you can see the difference because the homemaker, the assisted living you’re not, people are around but they’re not necessarily doing quite as much.

Nursing home care

When you move to nursing home care, now you have nurses who are caring for you, doctors, a lot more significant levels of care and it’s reflected in the cost. $7900 to $8,600 a month. And usually, with those in those costs are built-in some things like food— you know— the fact that you’re usually in a nursing home they’re providing your meals. You’re not driving out to McDonald’s to get your Big Macs or anything. They’re bringing you food.

Greg: They’ve got to be smuggled in.

Mark: Yes, and so, you know within that sort of all of your living expenses built into one. Almost twice as much as some of the others because you know at home you’re still paying for your mortgage. You’re still paying for your utilities. You’re still paying for all your food.

Once you move into the nursing home that’s pretty much where all of your expenses are coming from and. So a lot of time at home—

Greg: And if one of your spouses is at home still you’ve got this $8,000 a month outflow and you still got a house to run.

Mark: Right still have a house to run, still have he or she still has their food, you know, the utility bills are pretty much the electric build a cool house doesn’t matter how many people are in it?

Although it seems it seems the older you get the less cool you have to keep the house. Maybe that helps out a little bit, but those are—

Greg: So I was going to say obviously these are some pretty hefty expenses that were looking at. I mean we’re talking about anywhere from 50 to 100 grand a year, you know plus or minus for these different services. So if you don’t I guess the point that I’m making is if you don’t take these into consideration this could bankrupt you. I mean, this could wipe you out.

Mark: Absolutely, you see the nursing home, you know, we could probably say Okay, adult daycare and extra $1,500 a month. That’s you know, we can absorb that.

$8,600 or an extra $8,000 a month. You know, there’s not a lot of people who can say yeah, we can do that for an indefinite period of time and it won’t impact our retirement plans, it won’t impact what we might leave as a legacy to our children.

And and so the danger is saying the danger is not planning and—you know—if you could see we don’t have the ability to pay $8,000 a month pretty quickly, you know, you’re moving in with your kids or you know, it’s gone, you’re a Medicaid facility that may not be where you want to be.

Greg: Right and you know Mark, I’m sure you probably have some stats and figures and studies. But what are the odds that I’m going to need—you know—long-term care expenses? Whether it’s you know in-home or skilled? I mean, what are the odds that I’m going to face these expenses.

3. Will I need long term care?

Mark: The odds are that about two-thirds of women and about one-third of men are going to need Care at some point in time. And recently a lot of the long-term care insurance companies realize that in some of their pricing. It used to be that males and females paid the same premium. If you were 55, husband and wife paid the exact same premium and over time, they’ve realized and it’s not probably earth-shattering information that women tend to live longer than men.

I think we’ve known that for a long time. And what they realize is that because women are living longer than men they are more likely to be alone. And even though us men probably are horrible caregivers compared to our wives providing care for us men that when they were together the husband’s are helping with some of those things. And so you may have somebody who needs a little bit of care. And while the husband’s alive, he’s just doing it.

When he’s gone then she needs care. She starts using a policy for benefits. She starts going into an assisted living facility. And because her life expectancy is longer. I think I read something that 75% or 80% of the residents of nursing homes are women. So so recently they’ve adjusted the insurance companies most of them have adjusted so that female rates are higher for the same benefits than men because they’re much more likely to actually use the policy.

living facility. And because her life expectancy is longer. I think I read something that 75% or 80% of the residents of nursing homes are women. So so recently they’ve adjusted the insurance companies most of them have adjusted so that female rates are higher for the same benefits than men because they’re much more likely to actually use the policy.

Greg: Wow, okay —you know— and it makes a lot of sense the way that you described it because they live longer and because the man typically dies earlier the —you know— the husband’s going to be there to take care of her until he’s gone and then all of a sudden the wife is on her.

Mark: Right, right. And then yeah, it’s she moving back in with the kids. Is there a facility what’s that decision tree at that point that they didn’t have to make initially if she needed to care first.

4. How does long term care work?

Greg: Okay, so Mark —you know— this all sounds interesting and I want to start planning for this. You know, how does the whole long-term care process work?

Mark: Well, at least as far as the application process, it’s —you know— one of the things that we do is we work with a number of different companies to try to find the best fit and how we find the best fit is talking to the clients your clients the people who want to apply for the policy and we’re going to get a pretty detailed health information worksheet done on the clients because when you apply for the insurance, the insurance company is going to do what we call underwriting.

They’re going to look at a client’s application. They’re going to look at their medical records, prescriptions they may be taking. Summon long-term care insurance companies even have what’s called a paramedic exam where a nurse comes out and takes a blood and urine sample gets a height and weight if somebody hasn’t seen a doctor in a number of years and what I think is interesting is that.

A lot of times we’re used to or at least advisors are used to the underwriting for life insurance. Though they have this, they can’t get life insurance so they can’t get long-term care. It’s actually many times. It’s not sort of the opposite. Life insurance is looking at what are the chances of you dying too soon?

And so if the farther back somebody says I think they’re much more likely to die than the normal life expectancy that person might not get eligible for life insurance. The long-term care insurance is looking at the exact opposite. What are the chances of this person living too long? Living past normal life expectancy, living past where they’re able to care for themselves. So there are things like heart attacks that are much less of an issue for long-term care insurance than it is for life insurance because a lot of times it’s the second or third heart attack. It will kill you.

Greg: You’re just dead.

Mark: Yeah, you’re just dead. There’s no long-term care claim. Wherewith long-term care that’s not a concern to them, but something like another good example is MS. For long-term care. That’s a non-starter. It’s this person is, has a diagnosis of something that is almost certainly going to have some limiting effects for life insurance many times it’s not an issue may not get the absolute super preferred rates, but a lot of companies will look at a standard rate because that person’s life expectancy isn’t actually diminished all that much. But the ability to do things is potentially diminished quite a bit. And so you have a life insurance that’s normal long-term care, not eligible.

So back and forth between the two different things is the underwriting but in a home office underwriter reviews the application, medical records and then they make an offer standard. Hopefully, most of the time long-term care is the number of Ray classes is pretty small. With life insurance, you have a super preferred, preferred standard plus, standard, lots of different options. Long-term care insurance it’s usually your approved so it might have a preferred rate and a standard rate and relatively streamlined, and once you’re approved then the policy can be issued and you have to pay the premium which is the part that people like the least and the policies in place.

Greg: Okay, and so once it’s in place and for example in you know, my family situation, we were considering you know, what point do we actually pull the trigger and start taking some of these benefits, you know from that process walk us through you know the next few years and how that works.

Mark: Sure sure. So for a number of years hopefully nothing happens and you pay the premium depending on the design of the policy there may be some built-in annual increases and so the starting off at a $4,000 a month policy grows a little bit every year. So 10 years down the road it’s grown to $5,000 a month that you could use for long-term care benefits. Something happens and realize that ensured may need to be able to use the benefit.

So you contact either us, the agent or the home office directly and say, you know, my dad, my spouse, my whoever was recently diagnosed with Alzheimer’s and so we’re looking at how are we going to provide care, we have this policy how do we start doing this? And you essentially open up a claim and the insurance company is going to probably contact the doctor, get some of that information, look at the claim and what’s really neat about a long-term care policy is that you have what’s called a care coordinator. Let’s say that I don’t, my parents live here in Tampa actually about three blocks that way so it’s easy.

I would you know, if something happened to them, I would have some pretty good resource of where to go. But let’s say they live in Arkansas. I have no idea who a good home health care provider might be in Arkansas and the nice thing about working with with the long term care insurance company is lets say Mutual of Omaha, has providers who they’ve worked within the past and they’re getting feedback of ABC Home Healthcare was great, XYZ home healthcare not so great. So you have these care coordinators or people who they’ve worked with have alliances with to say, here’s some good Health Care, Home Health Care Providers, and you have that care coordinator where even if you’re far away, you can, kids or a spouse can help manage some of that as well.

Greg: So let’s just say that we start off with home health care and we’ve got somebody coming in to help out and do some of the —you know— cooking whatever that may be for 8 hours a day or whatever. That number is. At what point do you have to like refile a new claim to graduate into skilled care or something like that? How does it work?

Mark: Good question, no, once you qualify for needing benefits, you don’t ever have to qualify again. So people can come off of claim and then go back on but what happens is once you go on claim and let’s assume again something like Alzheimer’s where it just doesn’t get better then every month there’s a home health care provider, you’re paying the home health care provider the expenses, you’re sending the receipts to the insurance company and they’re reimbursing you for either how much you’ve paid or up to the policy limit. So let’s say that the policy benefit is $5,000 a month.

This month took to care of dad and the home health care bill for everything was $4,500. You pay the $4,500, submit the receipt to again the Mutual of Omaha, they reimburse for $4,500. Next month, something happened, needed some additional care and it was $5,500 this month. You pay the $5,500 to the home health care provider, send the receipt to Mutual of Omaha. They’ll reimburse $5,000 because that was the maximum monthly benefit for that policy.

Greg: Okay.

Mark: So what happens is in that first month that $4,500, that $500 you didn’t use that month stays in your pool. And so it sort of added on to the end. Sometimes I think that’s the long-term care insurance companies didn’t do a great job of defining policies by having years of benefits as compared to a pool of money. And so if you use less than the monthly benefit each month it stays in a pool and so you can get claims longer. You just are limited each month on how much you can use.

Greg:I did not know that you know, there’s a lot I don’t know about insurance and long-term care, but I did not know that so, you know a lot of people I think when they come in, they assume that I can only get long-term care for a certain number of years or periods of this month. And so what you’re saying is if you’re spending less than the policy Max that could drag out longer than whatever the policy says.

Mark: Absolutely. Like I said, we’ve defined it. I think however we are going far back. However far back the insurance companies defined it as $5,000 a month for three years. I think that’s easier for people to understand that then whatever $5,000 times 12 times 3 is $180,000 pool. When you think of it as $180,000 pool that I can get up to $5,000 a month. It makes more sense in your head to say. Well if I’m only using $2,500 a month this can last for six years, but the nomenclature is years three years, $5,000 a month and so I think that’s important is that anything you don’t use in any month sort of gets added on to the tail end.

Greg: Okay, and then to kind of circle back real quick, so I do have let’s just say at this point we have home health care and in a year, it’s really become overwhelming and we need skilled care. Does the Home Healthcare aide kind of send that up the chain to get you moved or how does that work?

Mark: No. No, at that point that can be a physician a doctor, that’s usually a doctor or somebody who’s making that call or it can be a spouse. I’m much larger than my wife. So if I was if it was hard for me to move around —you know— if I can move around by myself, and she’s watching me she may be able to care for me for a while. But at some point if she’s trying to pick me up —you know— actually move me around that’s more of a decision of I can’t do this anymore. Talking to the doctor. The doctor is probably going to say then yes, it makes sense to go to an adult daycare.

It’s usually more of a personal choice and to the insurance company. They’re not going to they’re not a gatekeeper to say no. We think you can stay home. So that’s what we’re going to do. There’s no there’s nothing like that. And that’s kind of what I was wondering if they were going to push back and make it real difficult.

Mark: Nope. Nope, and to them the longer that somebody’s may be able to stay at home, the smaller the claim so they’re going to help with that but they’re not in a position to say, right.

5. Who should consider buying long term care insurance?

Greg: Okay. All right. Well, that’s good to know. So —you know— tell me, Mark. I mean you deal with all kinds of people on a daily basis and you work with advisers who have a broad spectrum of clientele and life situations. Who should actually be worried or considering purchasing long-term care insurance?

Mark: I get this question a lot. And so I’m going to sort of Define it two different ways. One is financially and one is personal. Financially, I think people who have —you know— maybe a house and maybe four or five hundred thousand dollars of assets or less are probably not good candidates. They may be able to have it from an income flow perspective now, but if things change if, it’s not an inexpensive policy because like I said, it’s likely that you know third a third of men and I think two-thirds of women are likely to use this. It’s not, you know one in a thousand use it. It’s likely for people to use it. So the more likely they are to use it the more it costs when you have a benefit attached. So if your assets are too small.

Greg: You can wipe out your assets with premiums.

Mark: Right, exactly and that’s one of the things I look at. Is it going to change your retirement lifestyle if we add this premium? And if somebody says yes, then they’re probably not a good candidate because some point down the road if things change they’re going to look at this as unnecessary probably right at the time when they need it and so those people are probably more likely to be thinking about how we’re going to qualify for Medicaid.

Greg: Gotcha.

Mark: I’ve heard other things say people with a liquid net worth of $5 million dollars or more, you know, they could self-insure and I’d argue that they could but I’d argue why? Those are people who the premiums are affordable and I’d rather spend pennies to ensure dollars than to actually spend my own dollars.

So $5 million and over of actual liquid investable assets. I could argue they may be able to self-fund or do other things maybe use life if one of their concerns is leaving a legacy to their kids maybe use life insurance. That’s how we’re going to pass assets on to our kids and if we spend up all of our other money, that’s just fine and then anybody in those in those middles are great candidates. Because I’m kind of—

Greg: So anybody more than $500,000 to or liquid net worth $500,000 to $5 million you’re saying it’s a great candidate.

Mark: Yeah. Yeah, and because those, right and those yeah, the mass of fluent all of those are like you said if all of a sudden I have an extra $80 thousand of expenses that I wasn’t planning on it really moves the needle on things that we’re doing for retirement, especially if it happens to be an early onset of Alzheimer’s that let’s say age 68 my grandma Trimble actual blood relative Grandma had Alzheimer’s and lived a number of years and needed that Hands-On, Stand by, full care for years and you know so that can you think well, it’s just —you know— two or three years. It depends on what happens it can be, doesn’t have to be three years. So it’s that, you know financially is that to me it’s that sort of that range and

Greg: Okay.

Mark: Or as people wise —you know— I think the time when people really start considering it is early to mid-50s and there’s sort of two magical things about that age is one it’s about the time when people start having a family member who experiences it. Somebody has to care for mom or dad. You know, it’s hard. Sometimes it’s either when you’re really young it’s hard to think of your own mortality and hard to get a 26 year-old to buy life insurance.

Sometimes when you’re 40, long-term care that —you know— that happens to you know I’m not that old, but about early to mid-50s somebody’s caring for mom or your cousin is caring for your aunt, and it becomes a lot more real to you. And early to mid-50s is when we start moving I think people transition in their minds from financially and in my work and years I’m less can— before 50 or 55 I’m much more concerned about having enough to get to retirement.

Much more concerned about building it up. 50 to 55 I think something triggers in your mind 50 happens to be a nice round number and you start thinking more about how am I going to spend it in retirement and the long-term care helps prevent you from spending it too quickly. And so 50 to 55 I think is when people really start considering it, you know, I can talk to about long-term care to 32 year-olds all day long and it’s not real.

Greg: Now just out of curiosity though —you know— anecdotally a premium for a couple age 62, you know, they waited a little bit too long to get it is $5,000 a year or something like that?

Mark: That sounds about right.

Greg: And so if I was 40 years old and went to get this just for one person —you know— I imagine it’d be far less than half of that because you’ve got so many more years of me paying in before I’ll need it.

Mark: Right and yeah, and so that’s the one thing is if you do have the hard part with 30 year-olds is they probably also have child expenses, saving for college, student loan debt, all of these other things competing for all of their disposable income or hopefully they have a little bit of disposable income. And so yes if somebody’s doing really well with savings, high-income earners possibly it’s another great thing to look at, but usually when we start saying well and as you meet with younger clients, we need to add some life insurance because something happened who’s going to care for the kids?

We need to add some disability insurance because if you can’t work, none of these Financial plans work. That’s usually enough to make their palms a little sweaty. They thought they were doing great with their saving everything and then add long-term care is usually a non-starter.

6. How do you get long term care insurance?

Greg: That’s the death to the conversation. All right, Mark. So —you know— as I mentioned Wealth Masters, we both are affiliated with NAPFA and I kind of want to tackle this next question of —you know— how do I actually get started with a long-term care policy we briefly touched on it

But I kind of want a little bit more specific and —you know— how you work with NAPFA advisors because I know in the end you recommend that people find this and have this in the plan.

Mark: Absolutely. And so that’s you know by working with NAPFA planners, they’re looking at a client’s financial plan holistically and saying here’s all of the different things we’re going to look at. Here are the gaps we have. A lot of times what will happen is an advisor because NAPFA advisors are fee-only they don’t do insurance they will bring me into the conversation. It can be a phone call. It can be an email introduction. It can be a lot of different ways. Some advisors want to see initial premiums upfront to share with the clients.

Others already sort of have an idea of what it might look like and then ask the clients to contact us to do the underwriting interview. All of those are good options, but it’s something that the advisors have worked with the clients and set up and sort of had some of these conversations if you needed $80,000 for three or four years to pay for long-term care, where’s that going to come from and have you thought of it? What if you both needed the same time? Okay, here’s a way we can address that and solve that issue.

Greg: Okay. So in the context of an overall financial plan, it’s a good discussion to have with your financial advisor, assuming their comprehensive and a fiduciary. And then as far as a NAPFA fee-only advisor they might reach out to you and say hey Mark or somebody on you’re talented team. Hey Mark, you know, I’ve got this person over here. They’ve got an issue. Can you know, facilitate executing the long-term care.

Mark: Exactly, and we do. We get information about the client, find a policy that you know, A. meets their needs and fits their budget. We find out if there’s any health concerns. Is one company going to be more likely to offer them a policy than somebody else? And so we do a lot of that behind the scenes from let’s talk about this idea of long-term care insurance planning to here’s what an actual policy with premiums and benefits might look like.

Greg: Okay, and you know Mark as you mentioned that something just popped into my mind. Here’s a little Pro tip wealth Masters and I heard Mark say this at a conference not too terribly long ago when he was doing a very good presentation and —you know— just a circle back real quickly that care coordinator, because we talked about the expenses of long-term care premiums, that care coordinator which you had mentioned at that conference, was a lot of advisors are getting kind of a lower level or a base level long-term care insurance policy specifically just for that care coordination, right?

Mark: Right. and that’s part of what I look at with those different levels of costs. Some clients, some advisers say I’d like a policy that would cover those nursing home benefits. I want to know that I’m covered for all of that. A lot of advisors’ clients realize that their clients do have some assets. They do have social security coming in. Some have a pension.

It seems like fewer people have pensions than in the past, but I have assets I have other things so let’s have a policy that maybe doesn’t cover the $8,800 a month of you know needing the skilled care, but let’s have a $4,000 a month policy because that covers the home healthcare, covers all of the basics, you know covers a lot of different things and if I need to go into a skilled facility and its $8,800 a month well, I know that $4,000 a month is covered by the long-term care policy. I’m on the hook for that extra for the skilled care, but a lot of people transition from I can stay at home you know, I’m again I’m thinking of my wife caring for me initially.

She can help and then I might be able to stay at home and then the policy is going to cover all of those benefits. At some point, I might need to go into a skilled facility, but that’s usually a shorter period of time and that lowers the amount of benefits that have been covering a lot of different things and then sort of only there at the end where I need the skilled care. It’s still covering half of my expenses every month and then I’m just using my other assets for that additional.

Greg: Got you.

Mark: Some smaller amount to say no matter where I’m receiving care this is going to pay probably the full amount every month. It just depends on how much do I want to self-insure different levels of care?

Greg: Right, right. And as you mentioned that skilled care, which is double the $4,000 its $8,000, at least you’ve got $4,000 covered under kind of a base level policy and then you know, well, you know, maybe they need three months or a year of skilled care, but at least you’re limiting your liability personally.

Mark: Right right. Whereas if I could stay at home for two years before that, that policies covering most of what I need there.

Greg: Okay. Alright. So here’s a question that I get on a fairly regular basis when we talk about long-term care and can my premiums go up? Because I I’ve seen clients and that’s happened. I thought they were supposed to say flat.

Mark: Well, their traditional long-term care policies are what’s called guaranteed renewable. So it means that the insurance company can’t cancel a policy except for well, not paying premiums, but they have the ability to raise rates and what’s happened over time is that long-term care insurance is still the sort of the baby of all insurances out there. We’ve had life insurance policies for hundreds of years by now. Disability benefits and plans are built in decades and decades.

The long-term care insurance originally was just nursing home only facility and then they added some of these benefits like assisted living and Home Health Care not really knowing how people were going to use them or how they were going to build them in. So original policies were built-in with a couple of different things one where investment earnings which we know of come down laughs assumptions.

They assumed rates like life insurance that a lot of people don’t actually hold their policy till death on life insurance and they thought people were going to switch from different policies back and forth with long-term care and what you found is that.

People get older there’s not as good health and people are holding on to these policies. Almost I think it’s something like 99% of policies are being held till death. You just you get it and you hold on to it. And then the claims they didn’t really know how people were claiming. And so like I said here recently they’ve looked at some of the claims and said we need to charge women more than men.

They didn’t know that originally and so there have been rate increases. Nobody likes to see those. One of the things that I do because advisers come to us and say “Mark, my client has a long-term care policy. They got this notice of a rate increase. What should we do?” And I did one earlier this week client had a long-term care policy got it noticed that her premium was going up 20% from It was like a $1,000 a year to $1200 a year. That sounds scary, but the policy is a number of years old. She’s a number of years older.

To replace that policy today was going to be about $6,000 a year because the policy had what’s called inflation increases or these automatic inflation benefits, so she’d started off with a $100 a day $120 day it grown to a $180 a day automatically because she’d had it that long. So she’s now however many years older that was. The policy premium she had was building in those increases.

So it started a much higher benefit today and a much older age. Premiums are three or four times what she’s paying. So that’s how I like to frame it is that yes, it’s gone up, however, you can’t do it today for that much so as much as we don’t like that increase it’s a deal, you know, it’s worth holding on to and hopefully that’s where most people are talking to somebody and saying wow —you know— when you look how it compares to something else. It’s a fantastic policy.

Another nice thing that insurance companies do is that if they’re going to have that rate increase usually everyone that I’ve seen gives you a few different options and they say, okay the premiums going up from $1,000 to $1,200 a year. To keep your benefits exactly the same. It’s going to go up. If you’d like to keep your premiums at the thousand dollar-a-year levels. We could bring the benefit down from $180 a month $160. You know— what are some adjustments we can make to keep the premium level the same?

Greg: Extending the elimination period or something like that.

Mark: Yes extending the elimination period, maybe reducing the inflation amount, reducing the years of benefits. So all things that I think are very important because you’ve had this policy for so long you’re older now, you’re more likely to use it now than when you purchased it.

So find a way to keep it. Even if it’s reducing and you know in this scenario the advisor was very happy because the client was just going to pay the extra $200 a year. And when you see this —you know— quote unquote worth $6000 today for a new policy. You say wow. I’m going to hold onto that.

Greg: You would happily pay it.

Mark: Yeah, and some people —you know— may say well —you know— that is going to make a difference. Okay, let’s bring it down to you know, a 3% inflation instead of 5%.

Greg: Got it. Okay, so premiums can go up and if they do raise them to have to reason for everybody in that class, right?

Mark: Right. Yes, Yes. So the insurance company goes to the state insurance commission, says we have these policies that we issued between 1988 and 1990. We didn’t need to adjust the premiums because we haven’t had the lapses. We assume we haven’t had it. The State Insurance Commission actually has to approve these. They can deny them, the insurance company can in this case insurance company might have asked for a 25% rate increase and the insurance commissioner said well you didn’t justify 25% but the 20% is valid.

I don’t think that happens very often, but usually it’s then —you know— they have to show to the state that it is in order to keep the policy sound for everything for everybody that this is necessary and the state has to approve it and it’s usually done per state and it’s usually done on a what they call a block. So all policies issued between 1988 and 1990 and the 0735 policy Form. They can’t rule out Mark Maurer. They can’t rule out Greg Phelps.

Mark: They can’t pick out you or your mom or your uncle.

Greg: They can’t look at people who have had claims or you know people who are smokers when they took out the policies, they can’t do any of that.

It’s across the board here people who we may have to raise rates on and those are for additional traditional long-term care policies. There are other policies and we call them the hybrid long-term care policies. Either an annuity with long-term care benefits or a life insurance policy with long-term care benefits that do have guaranteed premiums, guaranteed benefit.

So those policies because they’re built on either a life insurance chassis you’re actually paying for life insurance and long-term care benefits are going to have higher premiums, but they can build in some of those guarantees knowing that if I pay my $5000 a year for 10 years, premiums can’t come back, premiums are going to be changed with the annuity. It’s a single premium policy and there’s a here’s what we projected but a guaranteed number. So there are options to add those guarantees, but today not on the traditional long-term care policies.

I will say that after looking at what insurance companies have done, the policies that are being issued today are the least likely to have future rate increases than anything before because we’ve had a continued low-interest-rate environment and insurance companies are pricing that in. They have a lot more claims experience —you know— so they’re building and more accurate claims experience.

They’ve also built in those laps assumptions to where they really are and not what they predicted so you know what the earnings have come down the lapse rate assumptions have come down, the claims experience has gone up and gone to gender pricing.

So today the policy today as a much lower likelihood of claims experience of having rate increases than anything in the past just because of where we are in time.

Greg: And they’ve got more data to make these decisions and to price and properly upfront.

Mark: Right and every year that goes by, it’s growing exponentially because every year that you add new policies, you’re also adding extra years to the policies in force. And so it truly is exponential growth on my claims experience on all of these different policies.

Greg: Right and I suppose Mark. I mean since the state insurance commissioner has to approve these rate increases it’s not like the insurance companies just going to go out willy-nilly and just try to —you know— jack up everybody’s rates. That’s a good thing.

Mark: Right.

Greg: And they have to go to the State Insurance Commissioner and say Hey, listen, we’ve had some Adverse Events in our pool and if you don’t let us raise our rates, we might not be able to stay in business.

Mark: Right and so from my understanding there’s a lot of times a lot of back and forth. It’s not a small thing to go in and ask for a rate increase. It’s a big deal. There’s a lot that you have to justify it. Probably six ways to Sunday and you know, there’s a lot of a lot that goes into it. A lot of justification like you said because if you don’t have good proof the State Insurance Commissioners definitely not going to let you do it.

Greg: Yes they will laugh you right out of the office. So I want to transition Mark and just a real quick question are my premiums tax-deductible? It seems like I’m making these premiums to help make sure I don’t go on Medicaid so the government should give me a benefit or something. Right?

Mark: Wouldn’t that be great? And let me grab some of my forms here because I’d like to say that I keep all of this in my head, but it’s not exactly. So for individuals and this is probably most people, an individual can deduct a little bit. And first, the IRS says you can’t deduct the full premium. So the IRS gives a table of how much of your long-term care premiums are actually deductible.

So let’s say that if you’re 50 between ages 50 and 60 the IRS says that you get to deduct up to $1,530 of your long-term care premium. No matter how much your premium actually was and in order for you to do that your medical expenses also have to exceed, I think it’s 10 % of your AGI, so you can’t it’s not a standalone thing.

That plus all of your other medical expenses, you have to be able to deduct a certain amount of medical expenses. I’m sure you know the words a little bit better than I do. But so—

Greg: You have jump through some hoops and—

Mark: Right.

Greg: It’s probably unlikely that you’ll get much if any of the tax benefit.

Mark: Right. Yeah, so you still have to have —you know— up to 10% of your AGI for paying for medical expenses. And then if you’re 55, you get to add $1,500 to that total number. So if that gets you to 11% AGI, you get a deduction of 1%.

Greg: Wealth Masters don’t plan on getting into deduction for it because it’s highly unlikely that you’re going to qualify for a tax deduct break.

Mark: And at least at the federal level a lot of states do have some additional benefits. If you’re in a state that has state income tax. I’m in Florida. I don’t so I have to admit that I don’t follow that as much as probably other states, and then we can go to almost the opposite and so for anybody who’s a business owner of a c-corporation, there are some fantastic tax deductions available. So a C-Corporation can pay the premiums for any employees or any owners.

The business gets to deduct it completely. It’s not included in the employees as an item on the employee’s income. Benefits received are still tax-free, you can pick and choose so you don’t have to like a lot of group benefits don’t have to offer it to everybody. So it’s really a win-win. It’s one of the few things that’s a win-win from every way that I can figure it out. You can even have the benefits be deductible for a husband and wife even if only ones an employee.

And so one of the few times when having and I know a lot of people like the escort for all the flexibility everything’s one of the few times when the C Corp actually gives you a little bit of flexibility.

Greg: Well, yeah because if you can if you don’t have to offer it and pay for it for every employee if you can pick and choose which to me seems very odd. I’m shocked that that’s even legal. And you can still write this off. I mean that’s amazing that makes it if you actually have a c-corp and a business and this is even remotely of interest to you doing this tour the sort of planning it’s well worthwhile to look into of course. We’re not offering tax advice. Please talk to your CPA.

Mark: I don’t know for tax advice either. So please talk to your CPA.

Greg: So, Mark, we’re going to kind of to bring it on home here with just a sample case that you’ve got here a proposal and this is going to stay on the screen for quite a bit and we’ll kind of reach of these if you could just kind of Hit the highlights just so we know if we get a proposal. What are we looking at?

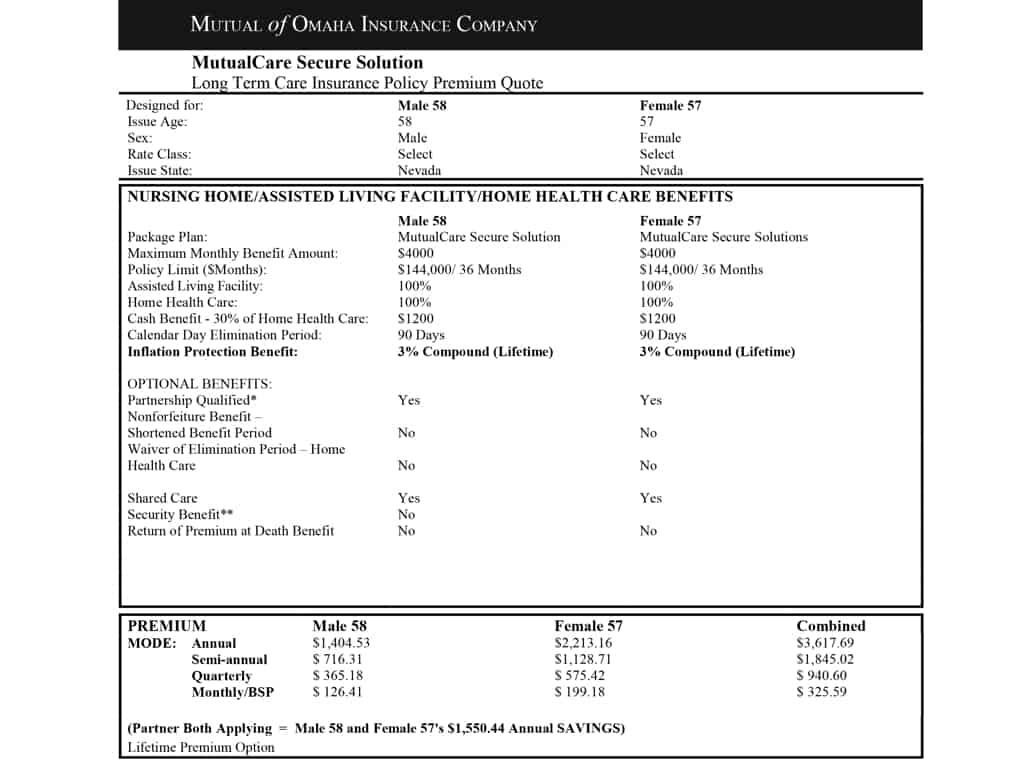

Sample long term care policy

Mark: Sure. Sure. So this is for a male 58 and female age 57 and so I’m just sort of looking at the benefits from the top to bottom. One of the things we’re looking at then is the rate class. So. You have sometimes the preferred rate classes the select or standard which in this case is select a sort of the normal, the average, the everybody kind of rate and then you see in the big box where it says nursing home, assisted living facility, adult day care, home health care benefits. So this policy is you can use the benefits for a nursing home, assisted living facility, Adult Day, Care Home Health Care, all of the different options. Some companies still offer a facility only plan, but we don’t recommend those and so this is just showing that this is traditional long-term care insurance policy and the maximum monthly benefit available $4,000 per month per person. So like I mentioned before if I use $2,000 a month I get reimbursed for $2,000 a month. And right below it that sort of helpful. There are policy limits of $144,000/ 36 months.

Greg: That’s that pool of money you were talking about that.

Mark: That’s that pool. So if the male age 58 used his benefits, for $4,000 a month exactly, it’s going to use up the $144,000 in 36 months. If he stayed at home and was able to have it be $2,000 a month, he’s using the $144,000 by $2000 instead of $4,000. So it actually lasts six years right below it. The that $4,000 is 100% available for assisted living or Home Health Care. This is a neat policy in that it has this cash.

And what it says is that in any given month, you can get reimbursed for up to $4,000 a month or you can choose to instead of that $4,000 a month get $1,200 in cash. Now unlike the reimbursement where if I use $2000 it stays in the pool. This is saying you’re giving up the $4,000 to get the $12,000. The extra doesn’t stay in the pool.

Greg: Okay.

Mark: But let’s say your daughter’s a nurse. Your daughter lives next door and she’s going to be able to care for mom or dad for a little bit. You have the ability to say, I’d rather she doesn’t work for a Home Health Care Facility. I want to have the cash so I can give it to her. And so that’s a nice option built into their elimination period. 90 days is the time when we haven’t talked about this yet, but the elimination period is a lot like a deductible on any other type of insurance. It’s usually defined with other insurance as a dollar amount.

This one is defined in a period of time. So if this male age 58 got diagnosed with Alzheimer’s on July 1st, he’s not eligible to receive benefits for 90 calendar days after that. So you self-insured the first 90 days. He or she is paying for the first 90 days of care out of pocket and then after 90 days then they’re eligible to start receiving benefits for that 36 months or until they use up the $144,000.

Greg: Okay.

Mark: And then right below it is the inflation protection benefit. This is a really neat component to a long-term care policy and that every year that goes by the $4,000 a month and that $144,000 pool is being increased by 3% on a compounding factor and why the 3%? Well, the cost of things long term care have been increasing somewhere in the 2-4% range every year. It’s sort of a health tire and it was 10 years ago. It was much higher and we usually looked at a 5% inflation option, but I think even though I think as people are getting older it’s more available and —you know— looking around here and —you know— when I go a little bit South to Sarasota, how many of the assisted living facilities I drive by and how nice they look. It’s a lot more available today.

And so the costs are going up about in that 2-4%. So we use the 3% so that that $4,000 a month is growing so that if I need care in 20 years, hopefully, it’s buying that same basket of goods that the $4,000 today did covering. It may have grown to $8,000 a month. But that’s maybe what that monthly for home health care and all those other things has grown too. So behind the scenes of the premium isn’t going up because of that, that’s just being, that are included in the cost and that’s being added to those monthly benefits every year.

Greg: Okay.

Mark: There’s a right below it optional benefits. There’s an asterisk next to partnership qualified. I could probably do another hour on what the partnership is. To try to make it brief a lot of states have a what’s called their partnership program that if you have a partnership eligible long-term care policy, so let’s say our male age 58 goes on claiming, uses up his $144,000 of benefits, if he applies to Medicaid, Medicaid says we’re going to exclude the first $144,000 from your asset.

So you get to keep $144,000 of assets before we start looking at how much money you really do have and how much you need to spend down Medicaid is really available for people who have spent down pretty much all of their money to sometimes $1,500- $2,000 dollars in total. So in this scenario, if he has a $144,000 in the bank, he can apply to Medicaid. They say you have a $144,000 in the bank.

However, because you used $144,000 from a partnership qualified long-term care policy, in essence, we’re considering that you have zero money.

Greg: Got it.

Mark: You get to hold on to that $144,000 because you’re self-insured and use this. Again, Medicaid is a two-pronged qualification. They look at income as well as assets. So like I said I could go on for another 45 minutes, but nobody would want me to so not going to.

Greg: We’ll save that for next time.

Mark: For part 2 if people are interested and then scrolling down a little bit farther to the shared care. This is something that I think is really neat for couples. And with shared care it allows those 36 months to be linked. So again to my average hot, cold, on average you’re comfortable. On average people use about 3 months or 36 months of benefits from their long-term care policy, but for every couple who use both exactly 36 months, there’s a lot more where probably one spouse uses a shorter period of time and one spouse needs a longer period of time.

So our male age 58 could use three years of benefits, his $144,000 and then be able to start using some of her benefit pool if he still needs care and so he can use her benefits leave whatever benefits are left over for her. I really want to see—

Greg: Essentially he’s got six years and of course she would have nothing but he’s now got six years.

Mark: Exactly. What’s another really neat component for this is that let’s say he never needs care. When he dies his benefits jump onto her policy. And her premium actually doesn’t increase from what’s down there in the below. So she gets to keep just her share of the premiums. But any unused benefits from his policy jumps onto hers. And so when we consider that most —you know— most women outlive their spouses may need care longer.

It’s a really neat thing that I think sometimes that isn’t highlighted well enough with a shared care benefit that, I don’t know if I’m going to need care but I am going to die one day and —you know— it’s much more likely for women need care men are more likely just keel over and die of a heart attack.

Greg: Chances are pretty good one of he’s going to need it.

Mark: Right right, and so in this case, but it’s —you know— it’s likely that he may predecease or he may use it for a short period of time or not at all. So then she’s alone and has all of his unused benefits and her premiums didn’t go up. It’s a really neat feature.

Greg: Good deal.

Mark: And then below there you see the premiums and that sort of highlights the differences that I mentioned she’s a little bit younger so, in theory, her premium should be a little bit smaller than his if they were gender-neutral but he’s a little bit older and his premium is quite a bit less because the likelihood of her going on claim is that much higher than him.

Greg: Okay, and so combined because they are under 60 little bit younger like we had used the example of me purchasing an insurance policy for long-term care, their premiums about $3,600.

Mark: Right and what you see right below that is the partner both applying insurance companies give pretty sizable discounts when two people apply together.

And so you can see that the $3,600 is actually $1,500 less because they both got a discount than if they were applying, if they were unrelated male 58 and female 57 because the insurance company says well because they’re together, if somebody needs claim, it’s likely that she can help with a claim —you know— if he needs care, she may do some of the health care herself and not need to start the benefits as quickly as somebody who’s alone or she might be able to provide care for some of the days and they only need a provider some other day.

So they’re looking at it as a husband and wife are much less likely to need a claim or to have somebody start a claim as quickly or as significantly as somebody who is just by themselves.

Greg: Okay, Mark real quick before we move on to this next part of The Proposal I guess. I’m just curious. I got to ask the gorilla in the room question what happens if I go and I buy one of these policies at 56 or 57, 58 with my wife and in 10 years we’re not married anymore. What happens to the policy?

Mark: The policy stays the same now, it comes down to depend on how amicable the separation was. You may not want her using your benefits if she goes on claim, but usually what happens is you can go to the insurance company, the partner discounts usually stay on, you can take off the shared care writer if desired.

Greg: And then split the premium up between the two of you.

Mark: I guess split the premiums up. Most of the time you use you keep that partner discount because that’s how it was.

Greg: Got it. Okay. Well, sorry just the gorilla in the room question in my mind. I’m thinking because I have clients and I’ve seen crazy things. So let’s kind of move on to this next slide here. And what are we looking at?

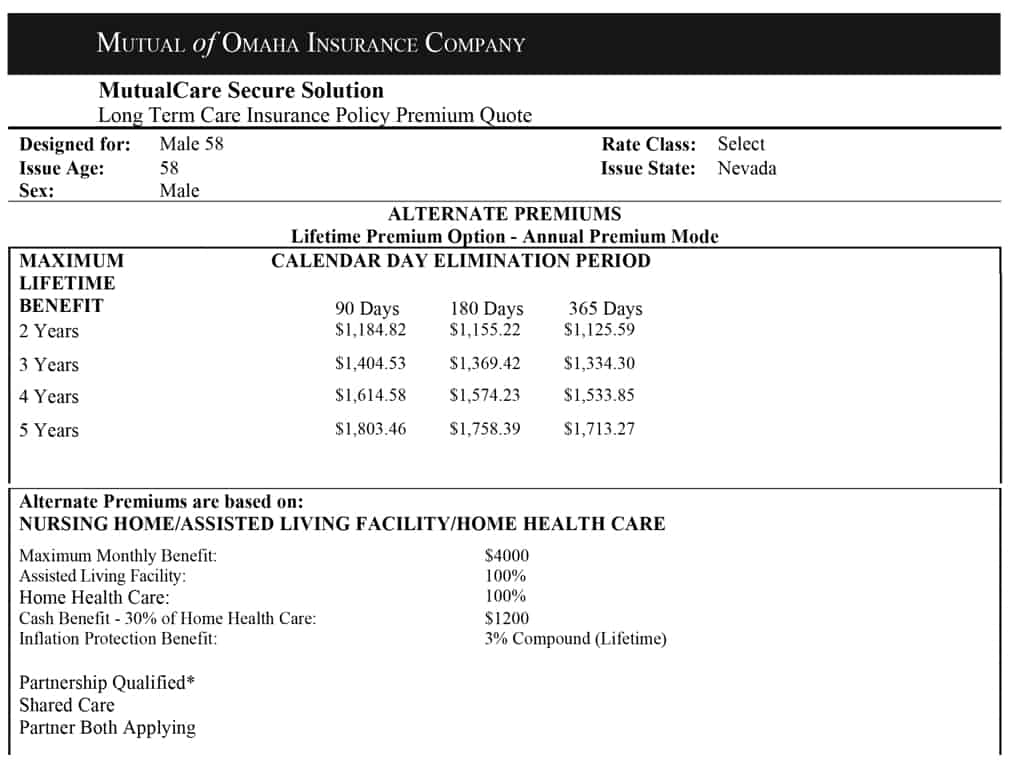

Mark: So here, so this is just for him. And so if you look at the 90-day sort of in the middle of the page where it says calendar day elimination period and it has the 90-day column and the three-year row, the 1404 is the same as what his share of the premium was going to be on the original page. So 90-day elimination period, three years of benefits.

Greg: Okay.

Mark: So this is highlighting how the premiums change if we change for him some of these specific factors. So as you said when we get the rate increases sometimes an option is to extend the elimination period so they could, if they wanted to, they could say we have enough money to self-insure for 6 months. Okay, then that reduces their annual premium of from $1404 to $1369. Not a significant decrease but a decrease is always a decrease.

Then to go to a 1-year limitation period brings it down again a little bit to $1334. What I always think is interesting and it makes sense. You would think that a 4 year benefit period should be twice as much as a 2 year benefit period, you would think that a 5 year would be, you know, quite a bit more well because you have a 2 year if it’s life insurance there’s just one event you die. Do I get $500,000 or a$1 million? That’s what it is because the length of the claim is undetermined. And you know if you Imagine everybody that goes unclaimed needs one month by definition, but a lot more people are going to need 2 years than they are going to actually get the 3 years and a lot more fewer people are going to use all 4 years.

NOTE: By the way, did you realize your kids may be responsible for your long term care expenses when you die?

So the incremental years are less and less because it’s less likely if you go unclaimed, you’re going to use some benefits initially, but the longer the claim goes the fewer people you have on the claim in the longer year. So adding 2 years you’re adding a year from 2 years to 3 years is a little bit more and it’s sort of incrementally more—

Greg: It’s not as much.

Mark: Right, right. It’s not doubling it for years, it’s not doubling two years because it’s not saying you’re going to get paid out for all four years.

Greg: Right and the likelihood of you needing it for 2 years is much greater than the likelihood of needing it for 5 years is probably very slim.

Mark: Right, right and insurance companies used to have some 10 year benefit periods, they used to have lifetime benefit periods. The lifetime benefit periods just started being too hard to quantify. If you give an actuary anything that has defined parameters, you can price it for insurance companies, but to say the claim is indefinite you can’t do, so how do you price that if you know with all the assumptions and how long people go and as long as there’s an end date they can do that.

So what we’ve seen is I think most insurance companies their maximum benefit period is a 5 or 6 year benefit period, those used to be lifetime benefits. Those are if someone has one those are again keepers, hold onto those, but it just became a how do you price something that has an Indefinite end date? You really can’t, you’re just guessing.

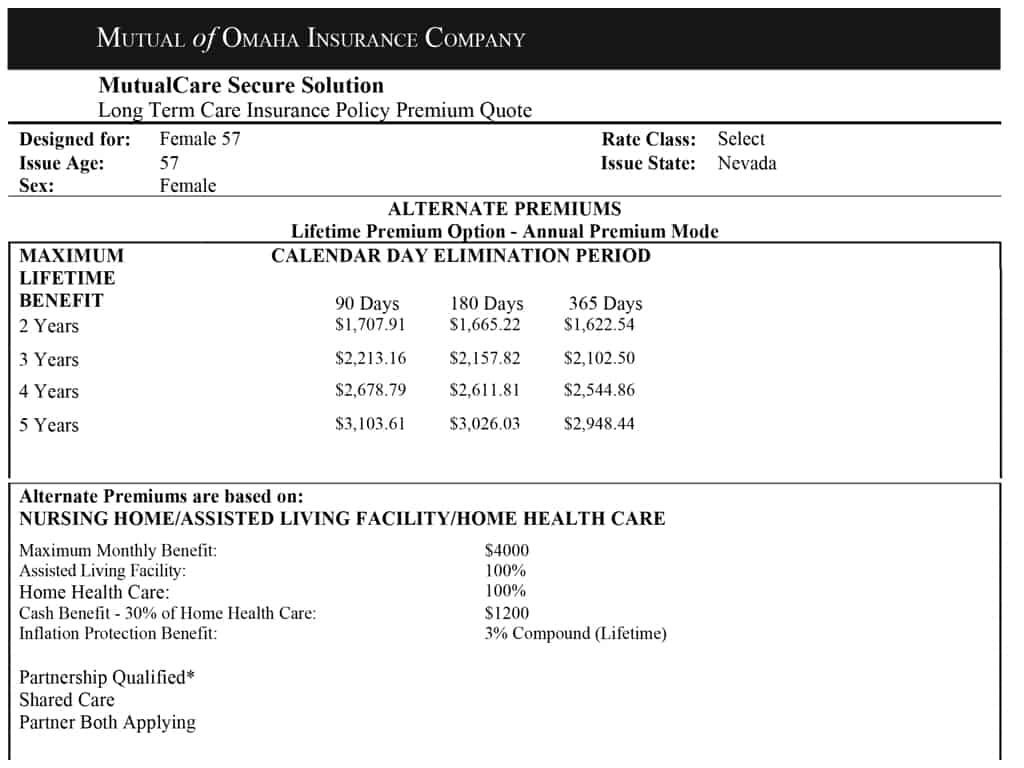

Greg: Got it and I see towards the bottom the expenses are all essentially the same as they were on that first page. I mean the expenses that, the notations for the maximum monthly benefit of $4,000 and assisted living that’s all the same as the first page and then I suppose the next page is actually just the same thing but for the wife.

Mark: The same thing for her exactly. So the nice thing about a long-term care policy is that if it was, so this changes the elimination period or the benefit period. If we wanted to change the monthly benefit period and keep everything else the same it is almost exactly proportional. So if we said for her we want to do the 90-day elimination period of 3 or benefit period but just $2,000 a month, her annual premium is going to be almost exactly half of $221,316.

I mean usually within pennies of that so that’s the, a lot of times with the quotes that part isn’t usually an optional page because it’s so proportional we can figure it out with our calculator and you don’t even need the fancy calculator. Just the good old, you know $4 Staples calculator. We could do those.

Greg: Yeah, I just bought my son both of my son’s a calculator for high school now and I think was $100. Each one of them was $100.

Mark: Was it a big graphing calculator?

Greg: It was exactly what it was. He looked at me and said look Dad I can graph stuff. I was like, well graph my heart that’s going like this when I spend $100 for a calculator.

Mark: All are the things that we need in school and then at the end of the day, what do you need really in life? You know? That.

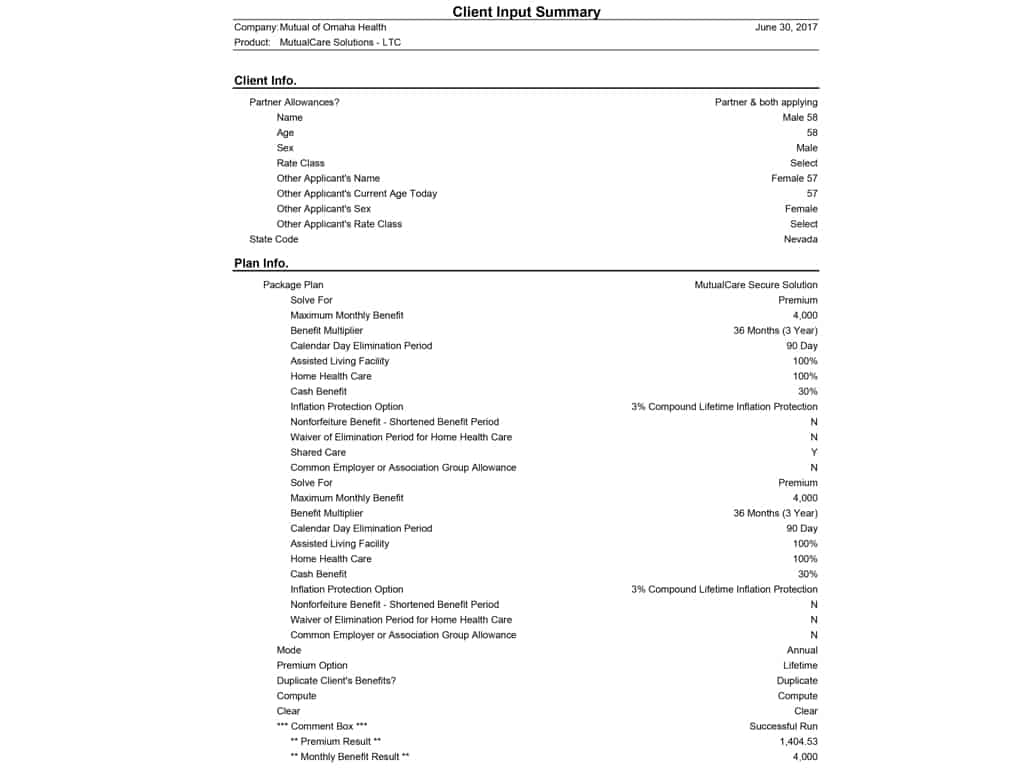

Greg: It’s crazy. Anyways, so Mark, I mean the next two pages and we’re going to link this on your speaker page. There’s just kind of the inputs that you plugged in to get the proposal.

Mark: Right, right.

Greg: Is there anything you’d like to touch on those?

Mark: No, no that —you know— this is just all the different sort of just the behind the scenes software programming that comes with all those inputs. It’s sort of this the same thing next page as well. Nothing really interesting in there.

Greg: Okay. Well Mark, let’s kind of bring it home. And what I like to say is if there’s just, you know, one or two or three critical things that the wealth Masters out there watching need to be cognizant of, they need to be thinking of and planning for and —you know— if there’s an action item or a takeaway, what are those main things that you want to share?

Mark: I think the first one was, I’m trying to remember in what order I said them to you now.

Greg: I think it’s the disaster —you know— scenario. What if you needed x amount of dollars $50,000 for long-term care, right?

Mark: Right. Yeah. Yeah, having that conversation and you as an advisor or everybody listening thinking in your head, where is that going to come from? What am I going to do? If if I have a group long-term care policy through work or I have my own policy, where is that money going to come from? Do I have $6 million dollars of liquid assets and A, I have some life insurance to make sure there’s money for my kids or I don’t have kids or don’t particularly like my kids and really care what happens to them.

I can’t imagine saying that, but —you know— so with that first question is when you start saying 50 to 60 thousand dollars per person a year, where is that going to come from? And then part two of that is okay that’s my first answer, what’s my backup plan? If that first answer is long term care insurance, that’s pretty good. You know— we’ve got that covered. We’re covering all those different things. What if my backup plan —you know— my initial plan is well, we’ll probably move in with the kids. Okay.

What’s the back-up plan to that if they say, you know, they got stationed overseas in Guam or maybe you know something horrible happens to them and they can’t care for you. What’s your backup plan? Is your backup plan Medicaid? Or maybe your backup plan was your kids. Those ideas I think usually get the conversation started because as parents we want to provide for our kids. We want to make sure they’re great.

You know, one of my goals is, my kids are 7 and 9, have a long time to worry about this but —you know— I want to not have had to rely on them when I’m older —you know— to let them be able to do whatever they’re doing and not have that burden to them, and then—

Greg: I think there’s a dignity thing that goes with it as well. You know— I think maintaining your dignity by being able to not or not having to go across town and it with —you know— with your suitcase and knock on the door at your kid’s house.

Mark: Right, right, exactly and —you know— the even having a long-term care policy, my kids may be helping with that care coordination. They may be —you know— doing some of that but they’re not doing is —you know— not lifting me —you know— out of bed or disrupting their lives their income-earning years, —you know— their primary income-earning years or trying to get kids through college all of those things to have to do with that. So, how are you going to fund that? What’s your backup plan? And then the third thing is do you have any and we call them sleeping dollars or sleeping money?

Cash values and an existing annuity that could be transferred to an annuity that provides long-term care benefits too. Existing life insurance policies that have cash values that could be transitioned to a life long term care hybrid. A lot of people have some Whole Life policies that they’ve built up over their working years. It was going to be money there if they have the death benefit in case something happened during their income years. As you’re getting close to retirement. There’s some money in there.

People say well, I’d really like to free up these premiums I’m paying. I don’t really have as much of the need for life insurance as I did when everybody was in college and I was working so reallocating the money in that life insurance policy to a policy that still has some life insurance benefits plus long-term care benefits can sort of solve two or three things all at once it can free up those premiums.

So my retirement spending numbers go down. Or can go up in more fun things. Hopefully, you know then have the death benefit there to pass on to my kids if I don’t need it and have that long-term care benefit if I never need it because —you know— as someone who’s a kid himself I would much rather have my parents be able to pay for things or have some life rather than worrying about leaving me something then vice versa.

And I don’t think there’s probably any kid out there who would say different but —you know— I would rather say if there are cash values there and —you know— it could provide $200,000 a long-term care or $100,000 death benefit —you know— as a child that just —you know— that would say that’s a mom dad that’s a great plan. It’s covering two different things because hey, I love you. I love it when you come visit. Not sure about If want you to live with me.

Greg: So Mark real quickly and that’s a whole other subject that hopefully, I can invite you back and —you know— for the next well Summit we can talk about that but real quickly so what you’re saying is there are life insurance policies. There are annuity policies out there that do have I guess maybe a writer for long-term care benefits something like.

Mark: Right, and that’s a touch on the hybrid. Those are the ones that have guaranteed benefits and there are even different flavors of long-term care. Some you can build to have quite a bit of death benefit where if you need care you get something like 2% of the face amount of the policy every month at a check. Once you qualify you just get that steadily.

Other plans are designed for a little bit of life in sort of minimal life insurance, but you can build the long-term care benefits to look like traditional long-term care policy. It’s going to have three, four, five years of benefits. I want the 3% inflation option on the long-term care benefits. So some are life insurance designed or sort of designed to maximize the life insurance component, but you could use it for long-term care if needed.

Others are designed more for the long-term care benefits, but keeping the life insurance component there. So that —you know— you’ll get you to know that you or somebody else will get some form of benefit out of it.

Greg: Right at least doesn’t feel so empty when you’re writing your $3,600 a year premium payment.

Mark: Right? Right, exactly you know that there are cash values there or I know you know, if I don’t use it, my kids get $100,000 if I need it. Then there’s $200,000 for long-term care benefits. Either way. Somebody’s getting something out of the $50,000 I put in.

9. Key takeaways

Greg: So I think what we effectively just did Mar is we took a very interesting and important topic and we made it a little bit more complex by throwing in these things at the very last key takeaways. Like I said stay tuned Wealth Masters we will get mark back on here. I promise you that.

Mark: I think I just booked myself another maybe two or three episodes doing all that at the end.

Greg: Yeah, I’m going to have to put you on payroll pretty quick. So I guess I would like to kind of some of —you know— in my opinion, being NAPFA advisor and a fee-only planner it’s very very important. There’s obviously a lot of considerations here and it’s a very very important topic. I will tell you that I don’t think that there is a single NAPFA financial advisor out there that doesn’t have the capability in the software to model.

For example, what Mark’s talking about, what happens if you have $50,000 or $80,000 at age 80 and you need to pay for your loss and care expenses for one to three years? What happens to your wife or your husband? What happens to your financial plan? And we can model these things through various software programs, just so you know how important this really needs to be to you.

10. How to reach Mark

So I would highly encourage you to reach out to a NAPFA a financial advisor and Mark —you know— at the end of every interview, I always ask our guests I say —you know— hey, how can our wealth Masters reach out to you if they want more information? You were gracious enough to actually send people to a nap adviser. Right?

Mark: Right, absolutely and our business was built exclusively by working with fee-only advisors and its really great for us because then —you know— I can talk about insurance. If somebody calls me I can give them guidelines on a long-term care policy, but. You know— just from a quick conversation I don’t have the ability to dive in like you do Greg or other NAPFA advisors to say here are all the different things they have going on in life.

How do we find something that fits —you know— more about what their budgets are, their needs are, their goals are and so we come in only when it fits there’s a saying “to a Carpenter every problem.” What is it with a hammer?

Greg: Everything looks like a nail.

Mark: Everything looks like a nail so —you know— to an insurance person a lot of times —you know— and insurance is the answer and if you call somebody and say I’m looking for a long-term care policy, they’re going to help with that, but it may not be the best fit. And so working with a NAPFA advisor we can find things like, oh they have this old annuity great. Let’s repurpose that to an annuity with long-term care benefits. Sort of does two different things at the same time.

So —you know— I would ask people to reach out to a NAPFA advisor to get that comprehensive plan. It’s like —you know— filling one chink in the armor, but if there are four or five other chinks, I don’t know it and so getting a NAPFA advisor to look at everything in the big picture is really helpful.