You’ve worked hard your whole life. You saved as much money as you could afford, when you could afford it. You funded your 401k’s and IRA’s as much as possible, because they were the best tool to boost your savings by lowering your taxes.

Now you’re retired or close to it. How do you turn your investments into spendable cash as efficiently as possible?

Only two things are guaranteed in life – death and taxes. Let’s focus on the tax part.

Retiring with pre-tax and after-tax accounts presents a big problem in retirement. You still owe ordinary income tax on your IRA’s and 401k rollovers, and taxes will eat up a big chunk of your assets. If you have any annuities, a portion of those are taxable as ordinary income as well!

We call spending down your investment accounts “decumulation”. Conventional decumulation wisdom says defer your taxes as long as possible. If you’ve got after-tax and pre-tax investment accounts, you should spend your after-tax accounts down first, followed by your pre-tax (401k and IRA type) accounts.

Conventional wisdom isn’t always best. Rather, strategies which help smooth your taxes over your lifetime may far surpass conventional wisdom.

What is tax smoothing?

Tax smoothing is a strategy to spend assets from different types of accounts in the most tax-efficient way possible. By drawing specified amounts from taxable and tax deferred accounts, you can stay within the most beneficial marginal tax brackets. By paying some taxes earlier rather than a lot later, you can minimize your lifetime tax burden.

Ask yourself where future tax rates will be? The United States is 19 trillion dollars in debt. Our economy is sluggish, historically speaking. The government needs revenue, plain and simple.

It’s possible – if not probable – that tax rates will rise in the future. This is a very scary proposition for the masses of baby boomers retired and retiring.

Let’s look at an overly simplistic calculation. Let’s say you’re married living on $75,000 per year you’re in the 15% tax bracket. The rough tax cost is $11,250 if it’s all coming from IRA’s and 401k rollovers.

If that 15% bracket jumps to 17%, the tax bite is $12,750. That may not seem like much, but the additional $1,500 in taxes is 2% of your overall income!

I don’t know about you – but to me – losing 2% of your income to additional taxes can be pretty painful. Smoothing your taxes – especially early in retirement – can yield dynamic results over your retirement lifetime.

Tax smoothing infographic

If you’ve followed the RetireWire financial blog recently, you may have noticed we love to create infographics! Infographics are a fun way to show tough money concepts simply.

If you’ve followed the RetireWire financial blog recently, you may have noticed we love to create infographics! Infographics are a fun way to show tough money concepts simply.

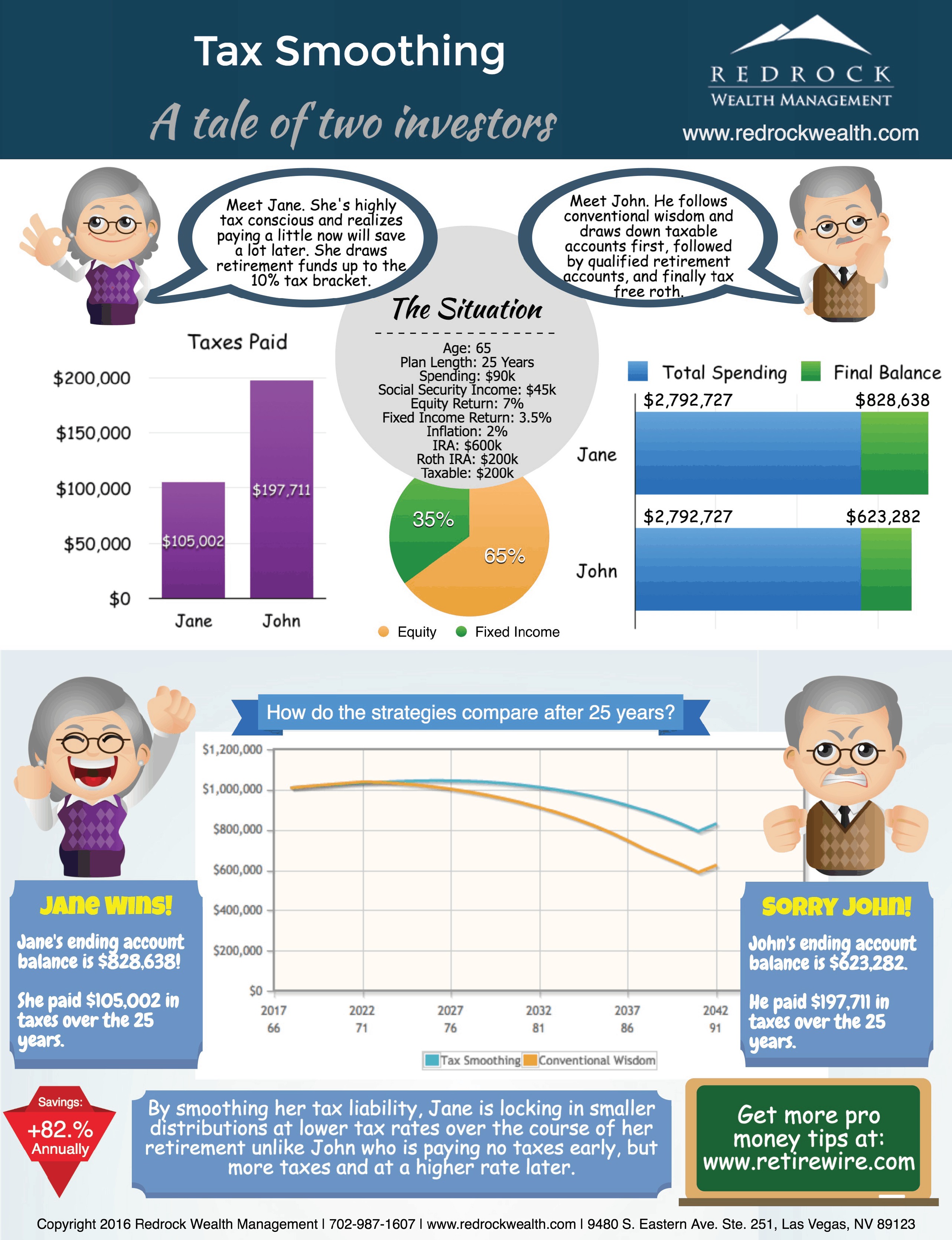

In our tax smoothing infographic, we used the income solver software. The situation is pretty simple. John and Jane are both 65 and the plan runs until they’re age 90.

Both John and Jane spend 90K a year, of which 45K comes from Social Security (from themselves and their respective spouse). They each have a million dollar investment portfolio in various taxable and tax-free accounts. Stocks earn 7%, bonds earn 3.5%, and inflation runs 2%. Both couples invest 65% in stocks and 35% in bonds.

The results are nothing short of spectacular! Jane and her spouse use tax smoothing strategies. They pay smaller tax amounts earlier in retirement, and less later in retirement.

John and his spouse use conventional wisdom. They defer paying taxes as much as possible as long as possible. John spends almost twice as much in taxes over his lifetime.

Calculating the actual return of tax smoothing

Because John paid so much more in taxes using conventional wisdom, his ending account balance is $623,282. Don’t forget, the tax dollars saved have a compounding effect over the 25 year plan period.

Jane smoothed her taxes throughout her retirement. Her ending account balance was $828,638 or about $200,000 MORE than John and his spouse had.

Jane paid less in taxes, so she died with more money. John paid more in taxes and died with less money.

We calculated the actual return Jane enjoyed for implementing a tax smoothing strategy in two ways. The first way is the actual tax savings.

Since Jane saved $92,709 in taxes relative to John, we used that amount divided by her original investment portfolio of $1,000,000. That’s a 9.3% improvement over 25 years. Annualized, that’s .37% over the 25 year plan period.

The second way we calculated the return from tax smoothing was the ending account balance. Since Jane’s investment portfolio ended $205,356 more than John’s portfolio, we divided it by the 1 million initial investment. That return was a bit over 20%. Annualized over the 25 year period, Jane made an extra .82% per year using this decumulation strategy.

How do you smooth your taxes?

Actually implementing this strategy is easier said than done. It requires complex tax calculations including several investment and return assumptions.

We use many pieces of software in our fee only financial advisor practice in Las Vegas. Each one has a different retirement planning purpose. One of them analyzes every reasonable combination of decumulation strategies and compares them side by side.

The software is called income solver. It produces a guide to the most efficient withdrawal strategy for clients. Part of the analysis is the investors age, income amounts and sources, and investment portfolio structure. The main part is the actual tax calculations behind varying distribution sequences.

If you have the time and money, the software is worth the investment. The amount you’ll save in taxes throughout retirement will far outweigh the cost of the software. If you don’t have the time and money, it’s very likely worth it to hire a fee only financial advisor who can produce these reports for you.

Outside of the income solver software, your accountant or CPA may be able to provide some guidance on tax smoothing. The philosophy is fairly straightforward after all, it’s the calculations that require the time and effort.

Tax smoothing in summary

The easiest way to boost your investment return is by saving taxes. Strategies such as Roth/IRA asset location and the strategic multi-bucket Roth conversion using Roth recharacterizations add tremendous value to your bottom line.

Tax smoothing is simply another way to save tax dollars throughout your lifetime. The more you save in taxes, the more you keep for yourself. And these are guaranteed dollars you’re saving – not investment returns which fluctuate from year to year.

If you’re not exploring tax smoothing strategies, you need to be. Talk to your CPA or find an excellent financial advisor to help you structure your retirement income as tax-efficiently as possible.